Sweden fresh fruit and vegetable market is built on imports, controlled logistics, and a small group of dominant wholesale suppliers.

Domestic greenhouse production plays a role in tomatoes, cucumbers and leafy greens. But the majority of fruit volumes entering Swedish supermarkets move through large-scale importers and distribution specialists.

Retail chains including ICA Gruppen, Axfood, Coop Sverige and Lidl rely on structured sourcing programmes. These depend on cold-chain precision, ripening capacity, packaging compliance, and predictable weekly flows.

In 2026, revenue concentration remains visible at the top of the supply chain. A limited number of companies control a significant share of organised fresh produce turnover in Sweden.

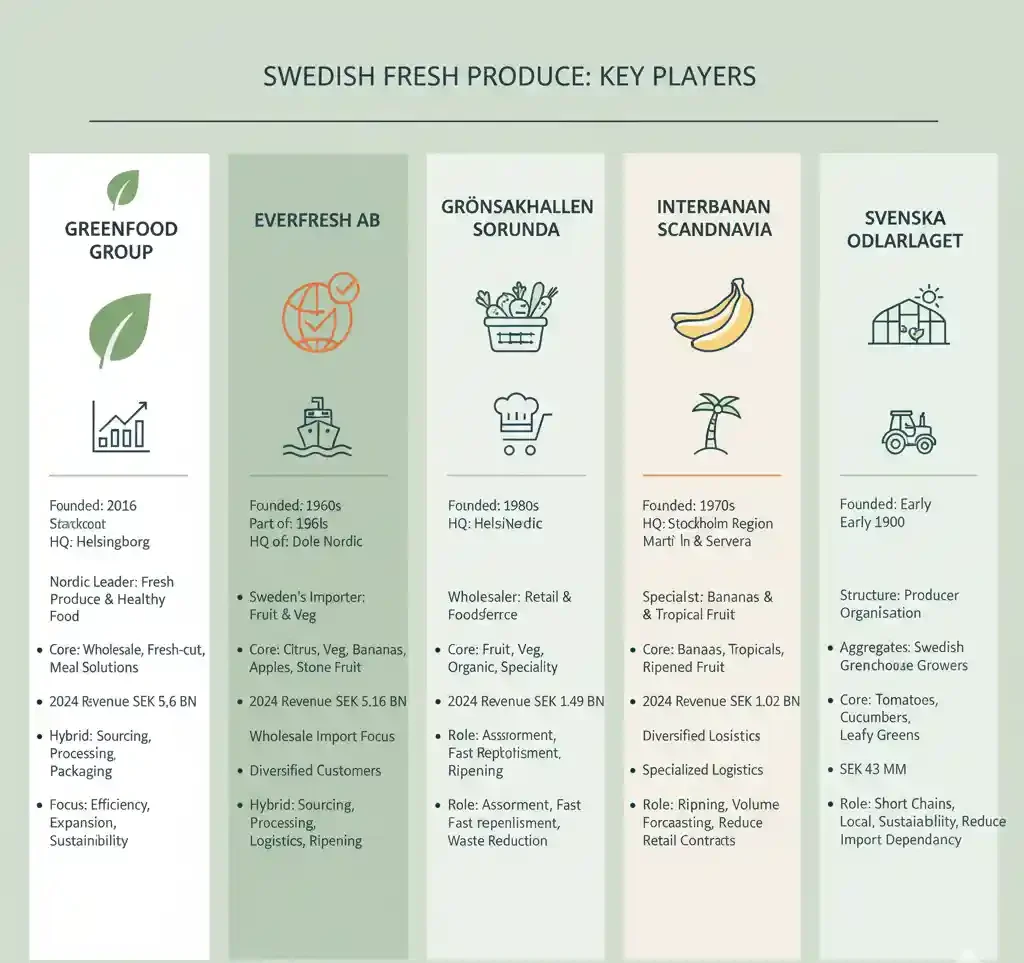

Revenue & Market Position (FY2024–FY2025)

| Rank | Company | Revenue (Latest FY) | Employees | Core Strength |

|---|---|---|---|---|

| 1 | Greenfood Group | SEK 5.6 billion (2024) | ~1,500 | Fresh produce + fresh-cut |

| 2 | Everfresh AB | SEK 5.16 billion (2024) | ~90 | Import & wholesale fruit |

| 3 | Grönsakshallen Sorunda | SEK 1.49 billion (2024) | ~500 | Retail & foodservice distribution |

| 4 | Interbanan Scandinavia | SEK 1.02 billion (2024) | ~14 | Banana & tropical imports |

| 5 | Svenska Odlarlaget | SEK 43 million (2024) | Producer organisation model | Swedish greenhouse crops |

Figures reflect publicly reported FY2024 or latest available financial disclosures.

1. Greenfood Group

Founded: 2016 (group consolidation roots go further back through legacy produce firms)

Headquarters: Helsingborg

Greenfood has grown into one of the largest Nordic players in fresh produce and healthy food solutions.

The group combines wholesale produce trading with fresh-cut processing, meal solutions and branded convenience lines. It operates across multiple European markets, though Sweden remains a core base.

Core product categories:

Whole fruit and vegetables

Fresh-cut salads and prepared produce

Plant-based food solutions

Retail-ready packed formats

Market position

With SEK 5.6 billion in turnover in 2024, Greenfood stands as the largest Swedish-headquartered fresh produce supplier by revenue scale.

Its integration of sourcing, processing and packaging gives it a hybrid position. It is not only a produce wholesaler. It is also a value-added operator.

Operational relevance

Greenfood’s structure reflects a broader industry shift toward:

Higher processing content

Retail-ready packaging

Convenience-oriented formats

This reduces shrink risk for supermarkets and increases margin potential per kilo.

Recent developments

Recent reporting highlights continued focus on operational efficiency and regional expansion. Sustainability initiatives and climate footprint management are increasingly embedded in supplier frameworks.

Greenfood represents the structural shift from commodity produce trade toward integrated fresh food solutions.

2. Everfresh AB

Founded: 1960s origins

Headquarters: Helsingborg

Everfresh is one of Sweden’s largest fruit and vegetable importers. It operates as part of the wider Dole Nordic structure.

Its model is focused on global sourcing and structured import programmes into the Nordic region.

Core product categories:

Citrus

Bananas

Apples and pears

Stone fruit

Seasonal vegetables

Market position

With SEK 5.16 billion in 2024 revenue, Everfresh ranks close to Greenfood in turnover scale.

Unlike Greenfood, Everfresh is more heavily weighted toward traditional wholesale import flows rather than fresh-cut production.

Operational relevance

Everfresh plays a central role in:

Year-round fruit programmes

Import scheduling

Ripening and handling systems

Port-to-distribution coordination

Sweden imports a significant share of fresh fruit. Everfresh sits directly in that gateway role.

Recent developments

The company has invested in digital ordering systems and operational optimisation. Efficiency in inbound logistics has become critical given freight volatility and energy costs.

Everfresh represents the classic high-volume importer model in Sweden’s produce supply chain.

3. Grönsakshallen Sorunda

Founded: 1980s

Headquarters: Stockholm region

Grönsakshallen Sorunda is part of the Martin & Servera Group. While Martin & Servera is known primarily for foodservice, this subsidiary operates as a significant fruit and vegetable wholesaler.

Core product categories:

Fresh fruit and vegetables

Organic lines

Specialty items

Foodservice-specific formats

Market position

The company reported SEK 1.49 billion in revenue in 2024, supported by approximately 500 employees.

It serves both retail and professional kitchen customers, giving it a diversified customer base.

Operational relevance

Grönsakshallen Sorunda’s scale supports:

Broad assortment depth

Fast replenishment

Mixed pallet solutions

Customised packing

It also plays a role in reducing waste through assortment planning and product utilisation initiatives.

Recent developments

Sustainability and local sourcing alignment have become more visible in recent years. The business operates within a cooperative-leaning ownership environment, which influences sourcing philosophy.

It is smaller than the two largest players but remains structurally important in the Stockholm region.

4. Interbanan Scandinavia

Founded: 1970s

Headquarters: Helsingborg

Interbanan specialises in bananas and tropical fruit imports. It is part of the Dole Nordic structure.

Core product categories:

Bananas

Tropical fruits

Ripened fruit lines

Market position

The company reported SEK 1.02 billion in revenue in 2024.

Its workforce is small relative to turnover. This reflects a highly specialised import and logistics structure rather than labour-heavy processing.

Operational relevance

Bananas remain one of the highest-volume fruit lines in Sweden.

Interbanan’s importance lies in:

Ripening capacity

Volume forecasting

Stable sourcing programmes

Retail contract management

Bananas are low-margin but high-volume. Efficient handling determines profitability.

Recent developments

Supply chain resilience has become more critical due to climate events affecting Latin American production regions. Specialist importers are increasingly required to manage volatility in yield and shipping routes.

Interbanan represents the commodity-specialist end of the produce spectrum.

5. Svenska Odlarlaget

Founded: Early 20th century cooperative roots

Structure: Producer organisation

Unlike the other four companies, Svenska Odlarlaget is not a classic wholesaler. It aggregates Swedish greenhouse producers and markets their output collectively.

Core product categories:

Tomatoes

Cucumbers

Leafy greens

Herbs

Market position

The organisation reported turnover of approximately SEK 43 million in 2024 at central level. Member farm revenues are separate.

Its scale is modest compared to import-heavy wholesalers. However, its structural importance lies in domestic production representation.

Operational relevance

Swedish-grown greenhouse vegetables support:

Shorter transport chains

Seasonal local programmes

Sustainability positioning

Lower import dependency

Domestic production still represents a minority of total fresh produce volume, but it plays a symbolic and commercial role.

Recent developments

Greenhouse technology investment, energy cost management and climate impact reporting have become critical. Swedish winter production remains energy intensive.

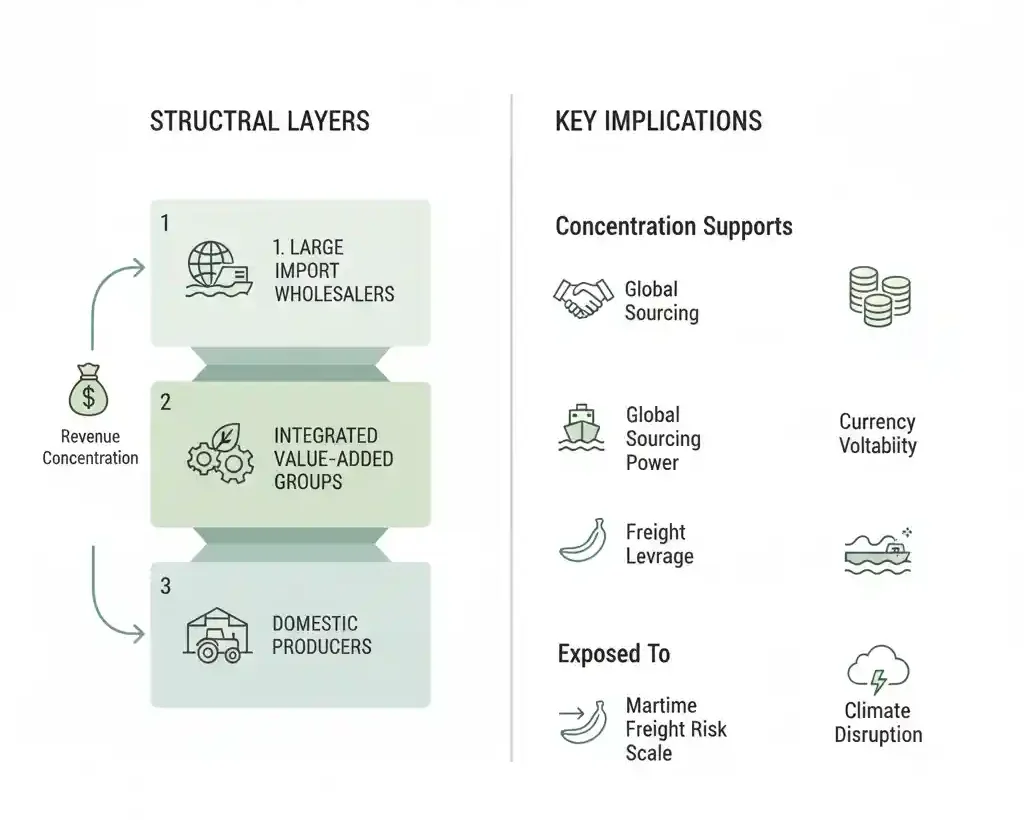

Market Structure Impact

Sweden’s fresh produce supply chain shows three structural layers:

Large import wholesalers

Integrated fresh-cut and value-added groups

Producer organisations and domestic growers

Revenue concentration is strongest in layer one.

The top two companies alone account for the majority of organised wholesale turnover among leading Swedish-headquartered firms.

This concentration supports:

Negotiating power in global sourcing

Freight contract leverage

Ripening infrastructure scale

However, it also increases exposure to:

Currency volatility

Maritime freight risk

Climate disruption in producing regions

Category Dominance Trends

Bananas, citrus and apples remain leading volume categories.

Vegetable lines show more fragmentation, especially in domestic greenhouse production.

Fresh-cut and prepared produce is gradually increasing in value share. Margin expansion often sits in these processed formats rather than bulk crates.

Private label penetration in Sweden remains high across supermarkets. That reinforces the importance of supplier consistency and contract reliability.

Industry Direction (2026 Outlook)

Several structural themes define the direction of Sweden’s fresh produce sector:

1. Logistics optimisation

Fuel and energy volatility continue to pressure transport margins.

2. Packaging compliance

EU packaging regulation and recycling targets influence retail-ready produce formats.

3. Climate risk management

Southern European drought cycles and tropical storm impacts affect supply security.

4. Local sourcing narratives

Domestic greenhouse lines retain branding importance despite limited volume share.

5. Value-added processing growth

Retail demand for convenience formats remains stable.

The industry is no longer only about moving boxes of fruit. It is about controlled freshness, packaging formats, shrink reduction and contract security.

Structural Change Outlook

Sweden’s produce market is unlikely to see dramatic new entrants at large scale.

Barriers include:

Cold storage investment

Ripening infrastructure

International grower networks

Compliance systems

Consolidation pressure may increase if margin compression continues.

At the same time, sustainability reporting and Scope 3 emissions tracking will place new data requirements on produce suppliers.

Supermarkets will increasingly evaluate suppliers not only on price per kilo, but on:

Carbon transparency

Waste metrics

Packaging recyclability

Delivery precision

Conclusion

Sweden’s fresh produce supply chain in 2026 remains concentrated among a handful of structured wholesalers and integrated fresh food groups.

Greenfood and Everfresh dominate turnover among Swedish-based players. Grönsakshallen Sorunda and Interbanan provide specialised and regional scale. Svenska Odlarlaget anchors domestic greenhouse representation.

The competitive edge is shifting from raw volume toward logistics precision, retail-ready formats and compliance-driven Sweden packaging standards. For Sweden supermarket operators, fresh produce remains one of the most operationally sensitive categories, where supplier scale, delivery accuracy and cold-chain control directly influence shelf stability and margin performance.

Editor’s Note: All financial figures are based on publicly available FY2024–FY2025 company reports and official disclosures. Revenues are stated in Swedish kronor (SEK). No currency conversions were applied.