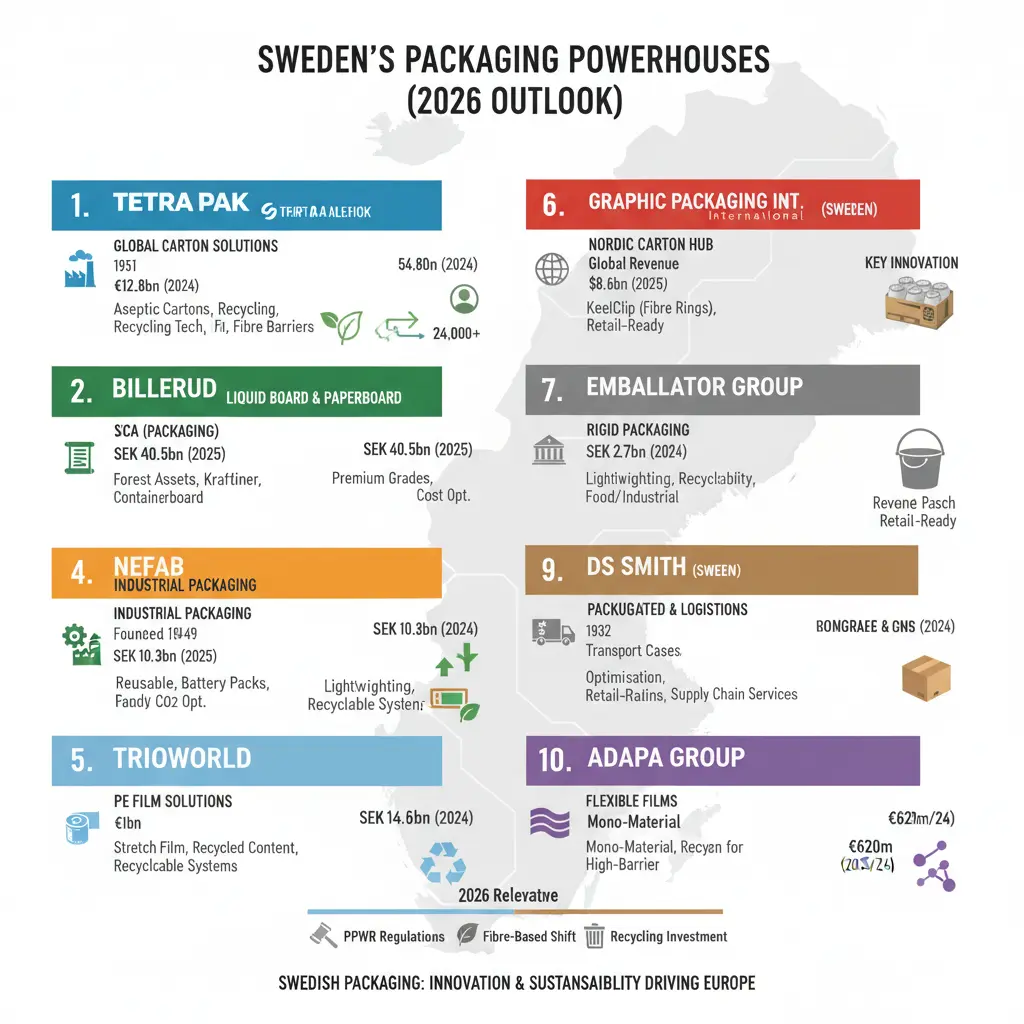

Final Revenue Ranking (Latest Reported FY)

| Rank | Company | Revenue (Latest FY) | Core Strength | Swedish Hubs |

|---|---|---|---|---|

| 1 | Tetra Pak | €12.8bn (2024) | Aseptic carton systems | Lund |

| 2 | Billerud | SEK 40.5bn (2025) | Liquid board & cartonboard | Gävle, Gruvön, Karlsborg |

| 3 | SCA (Packaging) | SEK 20.4bn (2025) | Kraftliner & containerboard | Obbola, Munksund |

| 4 | Nefab | ~SEK 10.3bn (2025 run-rate) | Industrial eco-packaging | Jönköping |

| 5 | Trioworld | ~€1bn (2024) | Flexible plastic film | Smålandsstenar |

| 6 | Graphic Packaging International | $8.6bn (2025 global) | Folding cartons | Lund (legacy AR ops) |

| 7 | Emballator Group | ~SEK 2.7bn (2024) | Metal & plastic rigid packs | Ulricehamn |

| 8 | DS Smith (Sweden ops) | FY2024 basis | Corrugated packaging | Mariestad, Värnamo |

| 9 | Boxon Group | ~SEK 1.6bn (2024) | Packaging logistics & labels | Helsingborg |

| 10 | adapa Group | ~€620m (2023/24) | Flexible food packaging | Landskrona |

Group-level revenues are used where Swedish operations are core. Currency conversions reflect average FY exchange levels.

1. Tetra Pak

Founded in 1951 in Lund, Tetra Pak remains Sweden’s largest packaging-linked business by revenue.

Revenue: €12.8bn (2024)

Employees: 24,000+

Core categories:

Aseptic cartons

Filling equipment

Processing systems

Recycling technologies

Lund remains a global R&D centre for beverage carton systems.

2026 relevance:

Ongoing work on fibre-based barrier materials

Efforts to reduce or eliminate aluminium layers in liquid cartons

Recycling infrastructure investment across Europe

Tetra Pak defines dairy and beverage packaging across Nordic and EU retail chains.

2. Billerud

Founded in 1855, Billerud is one of Europe’s leading producers of liquid carton board and specialty paperboard.

Revenue: SEK 40.5bn (FY2025)

The earlier SEK 43.5bn peak reflected stronger market conditions.

In 2025, weaker European demand and lower board prices reduced net sales.

Key pressures:

Oversupply in European cartonboard

Reduced Asian liquid board volumes

Price compression in standard grades

Core categories:

Liquid carton board

Folding box board

Kraft paper

Containerboard

Strategic direction:

Focus on premium specialty grades

Fibre-based barrier innovation

Cost optimisation amid demand slowdown

This demand pressure adds credibility to Sweden’s “dual-speed” packaging economy in 2026.

3. SCA (Packaging Segment)

SCA represents the structural backbone of Sweden’s fibre-based export model.

Revenue: SEK 20.4bn (2025)

Unlike converters, SCA owns forest assets.

This vertical integration secures fibre supply and energy input.

Obbola mill:

One of the most advanced kraftliner facilities globally

Significant recent expansion investment

Core packaging exposure:

Kraftliner

Containerboard

Packaging paper

SCA benefits directly from long-term fibre substitution trends.

4. Nefab

Founded in 1949, Nefab focuses on engineered industrial packaging.

Revenue: ~SEK 10.3bn (2025 run-rate)

Core categories:

Reusable transport packaging

Fibre-based industrial solutions

Wood and protective systems

Growth drivers:

Electrification supply chains

Battery packaging requirements

Lifecycle CO₂ optimisation

Industrial packaging demand remains structurally strong despite FMCG volatility.

5. Trioworld

Trioworld specialises in polyethylene film solutions.

Revenue: ~€1bn (2024)

Core focus:

Stretch film

Agricultural film

Industrial film

Recycled-content solutions

Flexible plastics face regulatory scrutiny under PPWR.

Trioworld’s strategic response:

Higher PCR integration

Development of recyclable film systems

Volume pressure remains visible in parts of the flexible segment.

6. Graphic Packaging International (Sweden Operations)

Graphic Packaging’s global revenue stands at $8.6bn (FY2025).

Swedish significance:

The AR Packaging acquisition consolidated Lund as a Northern European carton hub.

Key innovation:

Fibre-based “KeelClip” systems replacing plastic multipack rings

Retail-ready carton packaging

This places Swedish operations at the centre of fibre substitution efforts in beverage packaging.

7. Emballator Group

Founded in 1906, Emballator produces rigid packaging for food and industrial use.

Revenue: ~SEK 2.7bn (2024)

Core categories:

Plastic buckets

Metal containers

Industrial rigid packs

Strategic direction:

Lightweighting

Improved recyclability

Rigid packaging remains essential for niche food and industrial segments.

8. DS Smith (Sweden)

DS Smith operates corrugated facilities across Sweden.

Group revenue basis: FY2024 reporting.

Core categories:

Corrugated transport cases

Retail-ready packaging

E-commerce solutions

Corrugated demand links to private label and distribution efficiency.

9. Boxon Group

Founded in 1932, Boxon operates at the interface of packaging production and logistics.

Revenue: ~SEK 1.6bn (2024)

Core functions:

Packaging optimisation

Labels

Supply chain packaging services

Acts as a systems integrator rather than a raw material producer.

10. adapa Group (formerly Schur Flexibles)

Formerly Schur Flexibles, the company now operates as adapa Group.

Revenue: ~€620m (2023/24 public reporting)

Following restructuring after 2022 financial irregularities, adapa repositioned its strategy.

Focus:

Mono-material flexible films

Design for Recycling (D4R) solutions

High-barrier recyclable laminates

Flexible packaging faces structural adjustment in 2026 due to PPWR compliance.

Structural Themes in 2026

1. Dual-Speed Economy

High demand:

Fibre-based packaging

Kraftliner

Barrier innovation

Volume pressure:

Commodity board grades

Certain flexible plastic applications

2. Vertical Integration Advantage

SCA’s forest ownership provides cost and supply stability.

This is a structural advantage in volatile fibre markets.

3. Regulation-Driven Innovation

PPWR implementation phases increase:

Recyclability requirements

Carbon transparency

Material simplification

This benefits fibre innovators and mono-material specialists.

Sweden’s packaging industry in 2026 is defined by structural transition rather than expansion.

Fibre-based leaders retain strategic advantage.

Flexible producers are adapting under regulatory pressure.

Vertical integration and energy resilience shape competitive positioning.

For Sweden supermarket operators, packaging performance is now directly tied to private label strategy, recyclability compliance and cost control. At the same time, Sweden private label growth continues to reinforce demand for fibre-based formats, simplified material structures and retail-ready design aligned with EU regulation.

Revenue leadership remains concentrated among carton and board producers, with global scale anchored in Swedish engineering.

Editor’s Note : All financial figures are based on publicly available FY2024–FY2025 company reports and disclosures, including 2025 year-end reports released in early 2026. Currency conversions reflect approximate average exchange rates.

As of Q1 2026, the Swedish packaging sector is navigating a dual-speed economy: strong demand for sustainable fibre innovation alongside volume pressure in traditional flexible plastics during final PPWR implementation phases.