Romania packaging companies sits at the core of supermarket logistics, FMCG manufacturing, beverage production and export distribution. Corrugated board plants support national retail supply chains. Metal can facilities anchor beverage volumes. Recycled fibre and PET processors are increasingly shaped by the national Deposit-Return System (SGR) and EU Packaging and Packaging Waste Regulation (PPWR).

In 2026, revenue scale alone no longer defines leadership. Industrial capacity, material integration, recycling exposure and multi-site operational presence determine structural influence across the Romanian packaging ecosystem.

The ranking below reflects FY2024 publicly reported revenue of the primary Romanian legal entity only. No aggregation of group subsidiaries has been applied.

All revenues are reported in RON.

FY2024 Revenue Ranking

| Rank | Company (Legal Entity) | FY2024 Revenue (RON) | Primary Segment |

|---|---|---|---|

| 1 | Canpack Romania SRL | ~850–900 million | Metal beverage cans |

| 2 | Rondocarton SRL | 648.3 million | Corrugated packaging |

| 3 | DS Smith Packaging SRL | 431.6 million | Corrugated packaging |

| 4 | Ambro SA | 429.7 million | Paper & corrugated |

| 5 | Vrancart SA | 395.6 million | Paper & corrugated |

| 6 | Smurfit Westrock Romania SRL | ~350–400 million | Paper-based packaging |

| 7 | Romcarton SA | 285.9 million | Corrugated packaging |

| 8 | Romcarbon SA | 225.6 million | Plastics & flexible packaging |

| 9 | VPK Packaging SRL | 212.9 million | Corrugated packaging |

| 10 | Green Pack SRL | 186.8 million | Recycled PET packaging |

This table reflects single legal entities registered in Romania.

No combined turnover from related paper mills or affiliated SRLs has been included.

What Defines Packaging Leadership in Romania in 2026?

Three measurable indicators define structural influence:

Domestic industrial footprint (number of production sites)

Material integration (paper mill, recycling loop, aluminium sourcing)

Supermarket and FMCG exposure (transport packaging, beverage supply, protein packaging)

Corrugated packaging dominates structurally, but metal and recycled PET are gaining strategic weight due to regulatory shifts.

Company Profiles

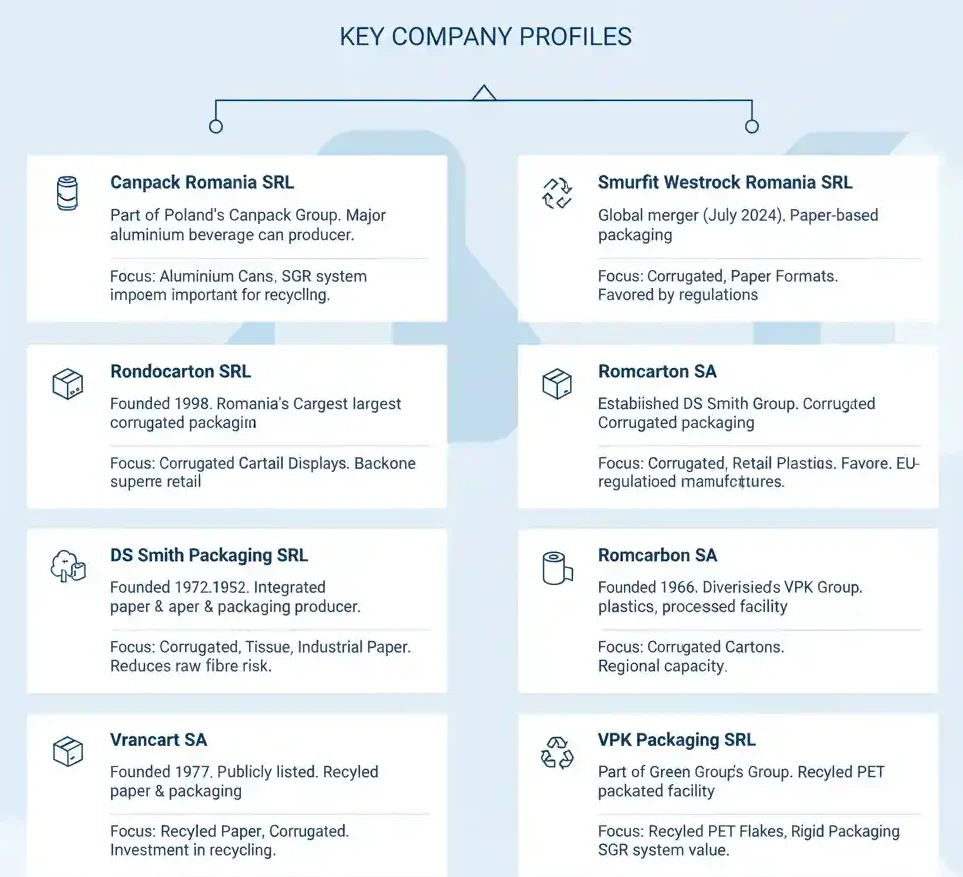

1. Canpack Romania SRL

Canpack Romania operates as part of the Poland-origin Canpack Group, founded in 1992. The Romanian facility is one of the group’s major beverage can production sites.

Core categories:

Aluminium beverage cans

Metal packaging solutions

The company operates a high-automation production plant serving multinational beverage producers in Romania and export markets. The aluminium can segment remains capital intensive but stable, supported by beverage demand.

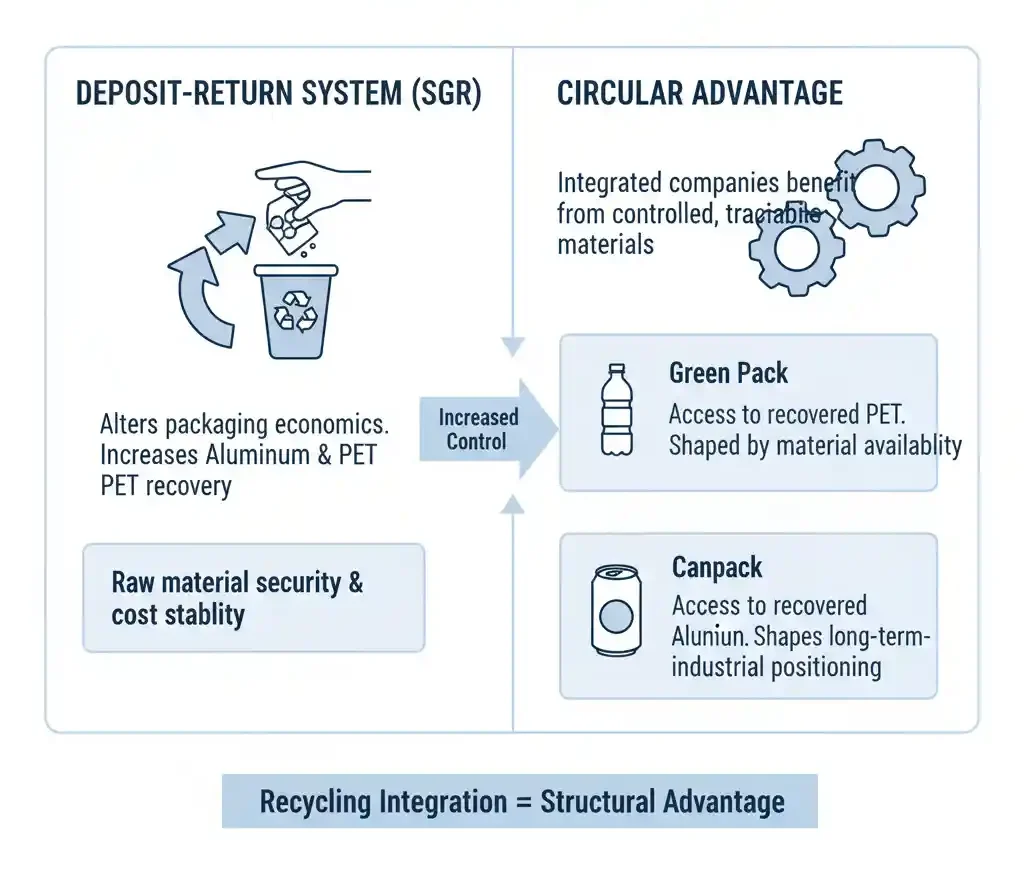

The SGR system increases the strategic importance of aluminium loop recovery. Material control now influences industrial leverage.

2. Rondocarton SRL

Founded in 1998, Rondocarton is one of Romania’s largest domestically active corrugated producers.

Core categories:

Corrugated transport cartons

Shelf-ready packaging

Retail display formats

The company operates three production plants. Its industrial footprint supports supermarket logistics networks and FMCG manufacturers requiring stable secondary packaging supply.

Corrugated remains the backbone of retail distribution in Romania.

3. DS Smith Packaging SRL

DS Smith Packaging SRL represents the corrugated conversion entity of the UK-origin DS Smith Group (founded 1940).

Core categories:

Corrugated packaging

Retail-ready formats

Industrial transit packaging

The reported 431.6 million RON reflects the packaging entity only. The larger paper mill (DS Smith Paper Zărnești SRL) is not included to avoid aggregation distortion.

The entity serves supermarket distribution centres and FMCG producers requiring high-volume corrugated solutions.

4. Ambro SA

Established in 1952 in Suceava, Ambro SA has evolved into a vertically integrated paper and packaging producer.

Core categories:

Corrugated board

Tissue paper

Industrial paper products

Ambro combines paper production with packaging conversion. This reduces exposure to raw fibre volatility and strengthens cost stability.

Its packaging division supports supermarket transport and private label distribution formats.

5. Vrancart SA

Founded in 1977, Vrancart SA is a publicly listed Romanian paper and packaging manufacturer.

Core categories:

Recycled paper

Corrugated packaging

Tissue products

Vrancart operates significant recycled fibre capacity. The corrugated segment supports FMCG manufacturers and supermarket distribution systems.

Investment in recycling infrastructure aligns with circular economy requirements.

6. Smurfit Westrock Romania SRL

Following the global merger in July 2024, Smurfit Westrock Romania SRL operates as part of the consolidated paper-based packaging group.

Core categories:

Corrugated packaging

Paper-based transport formats

The Romanian legal entity contributes to both domestic retail supply and export packaging networks.

Paper-based packaging benefits from regulatory pressure favouring recyclable materials over certain plastic formats.

7. Romcarton SA

Established in 1991, Romcarton SA operates within the corrugated packaging sector.

Core categories:

Transport cartons

FMCG packaging formats

While smaller in revenue compared to multinational operators, Romcarton maintains operational relevance for mid-sized manufacturers and regional contracts.

8. Romcarbon SA

Founded in 1956, Romcarbon SA is a diversified plastics processor.

Core categories:

Flexible packaging films

Polymer processing

Industrial plastics

Flexible packaging remains essential for protein, dairy and fresh produce categories. However, EU PPWR regulation is exerting structural pressure on plastic formats.

Romcarbon’s long-term direction will depend on recycled content integration and compliance adaptation.

9. VPK Packaging SRL

Part of Belgium-based VPK Group (founded 1935), VPK Packaging SRL operates a Romanian corrugated facility.

Core categories:

Corrugated transport cartons

The Romanian plant contributes to regional corrugated capacity, supporting supermarket and FMCG supply networks in specific geographic zones.

10. Green Pack SRL

Green Pack SRL operates within Romania’s Green Group recycling structure (founded 2002).

Core categories:

Recycled PET flakes

PET-based rigid packaging

With 186.8 million RON turnover in 2024, Green Pack is smaller in revenue but strategically important.

The SGR system increases PET loop control value. Recycled material availability now shapes industrial positioning more than pure revenue scale.

Market Structure Analysis

SGR and Circular Integration

Regulatory Pressure and Plastic Transition

Energy and Labour Cost Pressure

2024–2025 results show:

Labour costs rising across industrial sectors

Energy prices stabilised but above historical norms

Margin compression despite revenue growth

Packaging remains capital-intensive. Automation and efficiency upgrades are becoming necessary rather than optional.

Industry Outlook 2026–2028

Between 2026 and 2028, Romania’s packaging industry is expected to focus on continued optimisation of corrugated production capacity, expansion in recycled PET processing and sustained capital investment in automation. Integration with supermarket private label logistics is likely to deepen as retailers demand more reliable and compliant supply structures.

In this environment, industrial capacity will carry more weight than branding. Companies operating multiple facilities or maintaining control over raw material and recycling loops will be better positioned to manage cost volatility and regulatory pressure.

Conclusion

The top packaging companies in Romania by FY2024 revenue reflect a market structurally led by corrugated board production, supported by concentrated metal beverage can manufacturing and increasingly shaped by circular material integration.

Revenue scale determines ranking position, but industrial capacity ultimately determines long-term resilience. As the Romania supermarket network continues to expand and EU regulatory requirements tighten, packaging infrastructure remains a core pillar of supply stability, particularly as Romanian private label programmes increase demand for reliable, compliant and nationally distributed packaging solutions.

Editor’s Note: This article is based exclusively on publicly available FY2024 financial reports and Romanian company disclosures. Revenues are reported in RON. No group-level aggregation has been applied.