Portugal’s grocery market is one of the most concentrated in Europe. A small number of supermarket groups control most food sales across the country. While shoppers see many store signs, real power sits with just a few operators.

In this market, revenue matters more than store count. Scale, buying power, and operational control decide who leads. This ranking shows the five supermarket groups that dominate Portugal in 2026, and explains why they stay on top.

Top 5 Supermarkets in Portugal – Core Ranking

| Rank | Retailer | Revenue (Portugal) | Stores | Employees | Market Position |

|---|---|---|---|---|---|

| 1 | Continente / MC (Sonae) | ~€7.6bn | ~370 | Large national workforce | Market leader |

| 2 | Pingo Doce (Jerónimo Martins) | ~€5.1bn | 400+ | 30,000+ | Strong #2 |

| 3 | Lidl Portugal | Not disclosed | ~270 | Not disclosed | Leading discounter |

| 4 | Intermarché Portugal | ~€1.9bn | ~270 | Not disclosed | Regional strength |

| 5 | Mercadona Portugal | ~€1.8bn | ~60 | Not disclosed | Fast-growing challenger |

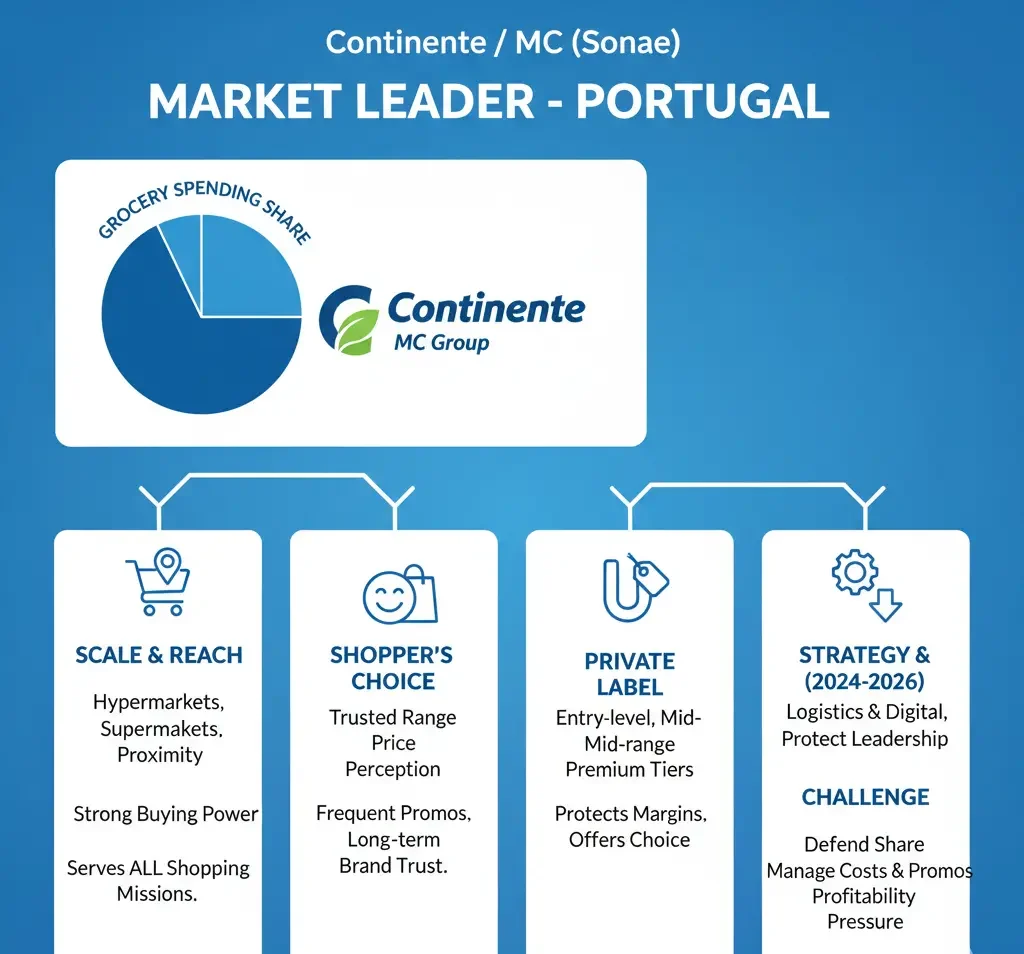

1) Continente / MC (Sonae)

Continente is the clear market leader in Portugal. It operates under the MC group and controls the largest share of grocery spending in the country.

Scale and reach

Continente combines hypermarkets, supermarkets, and proximity formats. This allows it to serve every type of shopping mission, from weekly family shops to quick top-ups.

Its scale gives it strong buying power. Suppliers depend on Continente for volume. This creates leverage in pricing, promotions, and contract terms.

Why shoppers choose Continente

Shoppers trust the range. Price perception is strong. Promotions are frequent and visible. Continente also benefits from long-term brand recognition in Portugal.

Private label strength

Private label is one of Continente’s biggest advantages. The retailer covers entry-level, mid-range, and premium own-brand tiers. This allows it to protect margins while offering choice.

Recent direction (2024–2026)

Continente continues to invest in store upgrades, logistics efficiency, and digital systems. The focus is less on rapid expansion and more on protecting leadership.

Key challenge

As market leader, Continente must defend share without damaging margins. Heavy promotions and rising costs put pressure on profitability, even at high revenue levels.

2) Pingo Doce (Jerónimo Martins)

Pingo Doce is the second-largest supermarket group in Portugal and the strongest direct competitor to Continente.

Scale and model

Pingo Doce runs a dense national network with strong central control. Its stores are well integrated into neighbourhoods and urban areas.

The group benefits from the wider Jerónimo Martins organisation, which brings experience from multiple European markets.

Why shoppers choose Pingo Doce

Fresh food is a major driver. Ready meals, bakery, and daily essentials are central to its offer. Shoppers also respond well to its promotional rhythm.

Private label role

Private label is deeply embedded in Pingo Doce’s range. It focuses on everyday categories where shoppers are most price sensitive.

Recent direction (2024–2026)

The retailer has focused on price competitiveness, loyalty offers, and operational efficiency as Portuguese households remain cautious with spending.

Key challenge

Cost pressure is the main risk. Labour, energy, and logistics costs continue to rise. Maintaining value without losing margin is a constant balancing act.

3) Lidl Portugal

Lidl is the strongest discounter in Portugal and a permanent pressure point for the full-line supermarkets.

Scale and efficiency

Lidl’s store network is large and well distributed. Its simplified model allows for fast decision-making and strong cost control.

The company does not disclose Portugal-only revenue, but its market share places it firmly in third position.

Why shoppers choose Lidl

Price is the main reason. Shoppers also trust Lidl’s quality for core products. The limited range makes shopping fast and predictable.

Private label dominance

Private label is the backbone of Lidl’s business. This gives Lidl full control over pricing, packaging, and supply terms.

Recent direction (2024–2026)

Lidl continues to modernise stores and invest in logistics. It also works to improve perception around quality and sustainability.

Key challenge

As Lidl grows, complexity increases. The risk is losing cost discipline while trying to compete more directly with full-range supermarkets.

4) Intermarché Portugal

Intermarché occupies a distinct position in Portugal’s grocery market. It is not built to dominate nationally, but to perform strongly at regional level. This makes its role very different from the large centralised chains.

Scale and operating structure

Intermarché operates a wide store network across Portugal, with particular strength outside major urban centres. Many stores are locally operated, which allows faster decision-making on assortment, pricing, and local sourcing. This structure gives Intermarché flexibility that larger groups often lack.

Why shoppers choose Intermarché

In many smaller towns, Intermarché is part of daily life. Shoppers value familiarity, proximity, and a store that reflects local preferences. The retailer benefits from long-standing relationships rather than heavy national advertising.

Private label and local mix

Private label plays a role, but it is not dominant in the same way as at Lidl or Mercadona. Intermarché often combines own-brand products with local and regional suppliers. This approach supports differentiation and strengthens loyalty, especially in non-urban markets.

Direction from 2024 to 2026

Rather than pushing rapid expansion, Intermarché has focused on improving existing stores, refining operations, and protecting its regional base. The strategy is about stability and relevance, not scale at any cost.

Key challenge

Intermarché faces pressure from both sides of the market. Discounters pull value-focused shoppers downward on price, while national leaders use buying power and promotions to defend share. Maintaining margin and relevance in this middle position is the central challenge.

5) Mercadona Portugal

Mercadona is the newest large supermarket operator in Portugal, but it has already become one of the most disruptive forces in the market. Despite having a much smaller store network than long-established rivals, it has reached revenue levels close to Intermarché in a relatively short time.

Scale and growth model

Mercadona’s performance is driven by high sales per store, not rapid footprint expansion. Each new location is designed to reach maturity quickly, supported by centralised logistics and tight range control. This model allows the company to generate strong turnover with fewer sites.

Why shoppers choose Mercadona

Shoppers are drawn to consistency. Store layouts are predictable, shelves are well stocked, and pricing is stable. The shopping experience feels efficient and calm, which builds trust and repeat visits. Mercadona also benefits from a reputation for good quality at fair prices.

Private label at the core

Private label is not an add-on for Mercadona. It is the business model. Own-brand products dominate the assortment, giving the retailer control over pricing, packaging, and supply planning. This reduces reliance on branded suppliers and supports margin stability.

Direction from 2024 to 2026

Mercadona has continued to expand in Portugal, but in a measured way. The focus is on operational execution, staff training, and supply chain reliability rather than fast store roll-outs. Growth is planned, not rushed.

Key challenge

As the network grows, complexity increases. Logistics costs rise, competition becomes more local, and expectations increase in new regions. The main challenge is maintaining the same operational discipline and store performance as the footprint expands.

How Market Power Really Works in Portugal

Why Private Label Keeps Growing

Private label is no longer a secondary option. In Portugal, it is a core strategy.

Retailers use private label to:

Control pricing

Reduce risk from branded suppliers

Respond faster to demand changes

Protect margins

Shoppers trust own brands more than before. Quality gaps have narrowed. Switching is easy.

This trend is structural and will continue beyond 2026.

Promotion Pressure and Margin Risk

Portugal is a promotion-heavy market.

Frequent discounts help volume, but they weaken margins. When all major players promote at the same time, price differences disappear.

Retailers then depend on:

Private label

Logistics efficiency

Data and systems

The largest groups manage this better. Mid-sized players feel the pressure more sharply.

Urban vs Regional Dynamics

| Area type | Shopper focus | What performs best |

|---|---|---|

| Urban areas | Speed and convenience | Smaller and proximity formats |

| Regional areas | Weekly shops and familiarity | Local presence and larger stores |

What Suppliers Must Understand

Portugal is not an easy supplier market.

Volume is concentrated. Negotiations are tough. Retailers expect flexibility and reliability.

Suppliers must be:

Cost competitive

Promotion ready

Open to private label

Operationally strong

Brand power alone is not enough.