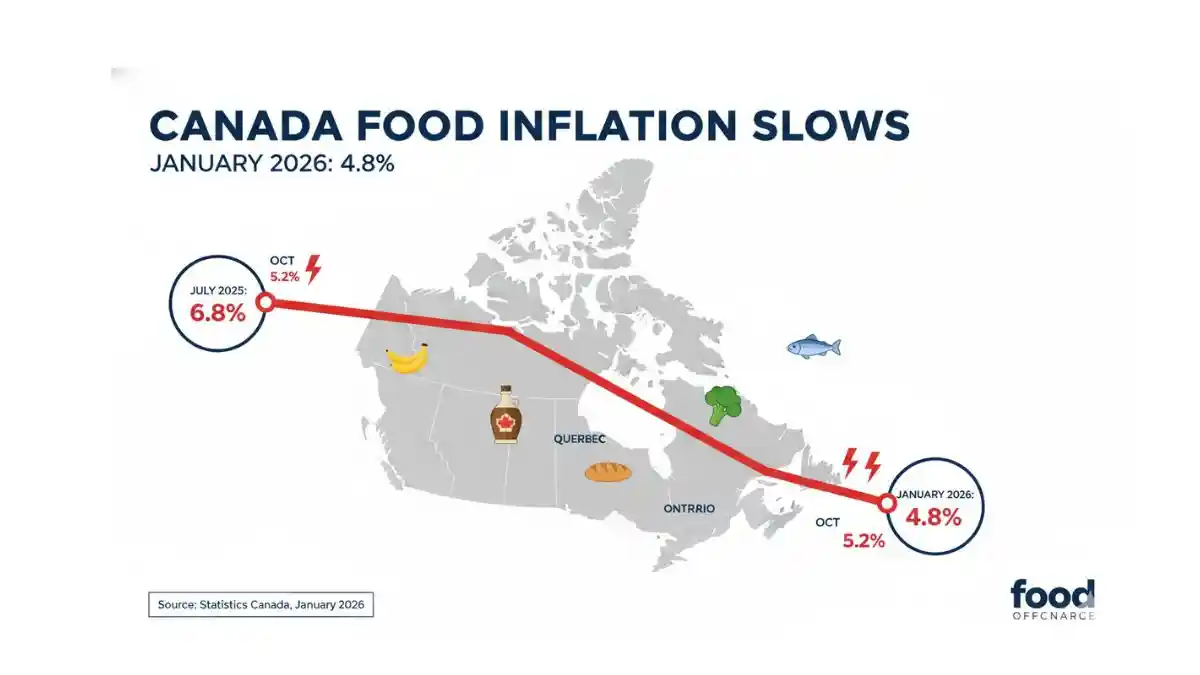

Canada food inflation eased slightly in January 2026, but grocery price growth continues to run well above headline inflation, keeping pressure on supermarket pricing strategies across the country.

Official data released on 17 February 2026 shows food purchased from stores increased 4.8% year over year, down from 5.0% in December.

By comparison, overall Consumer Price Index (CPI) inflation stood at 2.3%, confirming that grocery prices remain rising at more than double the national average.

The gap between food inflation and headline CPI remains wide — and structurally important for retail negotiations.

Key inflation numbers supermarket buyers should track

| Inflation Measure | January 2026 | December 2025 | Why It Matters |

|---|---|---|---|

| Food purchased from stores | 4.8% | 5.0% | Direct supermarket price pressure |

| All-items CPI | 2.3% | 2.4% | Macro environment |

| CPI excluding food & energy | 2.4% | 2.5% | Underlying inflation trend |

| Fresh fruit | -3.1% | +4.5% | Produce deflation driver |

| Gasoline | -16.7% | -13.8% | Logistics cost relief |

The moderation in food inflation is measurable — but limited.

At 4.8%, grocery price growth remains elevated relative to historical norms.

The real drivers behind January’s food inflation shift

The primary moderating factor was fresh fruit.

Fresh fruit prices declined 3.1% year over year, reversing December’s 4.5% increase. Statistics Canada linked the decline to stable or strong harvests in key producing regions.

Berries, oranges and melons contributed most to the downward movement.

This is important for produce-heavy banners and fresh-led retailers. Fruit deflation can support volume recovery, particularly in high-frequency traffic categories.

However, broader food pricing remains firm.

Restaurant prices rose 12.3% year over year, largely due to a base effect tied to the temporary GST/HST break in early 2025. Alcoholic beverages recorded similar base-driven increases.

These distortions affect CPI optics but do not reflect fresh structural shocks in 2026.

Headline inflation vs grocery reality

| Metric | January 2026 | Buyer Interpretation | Wholesale Impact |

|---|---|---|---|

| Food inflation | 4.8% | Elevated | Continued supplier pressure |

| All-items CPI | 2.3% | Moderating | Improves consumer sentiment |

| Gasoline | -16.7% | Cost relief | Logistics easing |

| Shelter | +1.7% | Slowing | Budget stability improving |

While energy and shelter inflation are cooling, grocery inflation remains comparatively sticky.

For supermarkets, this divergence matters more than headline CPI.

Food pricing affects weekly basket visibility, promotional intensity and private label switching behaviour.

Why grocery inflation remains sticky

Unlike headline CPI, which is being cooled by energy deflation, grocery inflation reflects:

-

Ongoing supplier margin rebuilding

-

Packaging and processing cost carryover

-

Labour cost adjustments

-

Currency exposure in imported food categories

Gasoline price declines provide some logistics relief. However, structural food production costs remain elevated compared with pre-2022 levels.

Excluding gasoline, CPI rose 3.0% — highlighting that underlying inflationary pressure remains higher than headline numbers suggest.

What factory and supply trends suggest

Although Canada’s Producer Price Index data varies by sector, food manufacturing input costs have shown uneven moderation.

This creates a negotiation environment where:

If factory costs fall faster than retail prices, retailer margin expands.

If supplier input relief is limited, cost claims remain firm.

January’s CPI data does not signal a collapse in supplier cost pressure. It signals gradual normalization.

That distinction matters in ongoing pricing discussions.

How Canadian supermarkets are responding

Retailers continue balancing cost recovery with price competitiveness.

Observed responses across the market include:

-

Continued expansion of value-tier and entry private label

-

Targeted promotional activity in fresh and high-visibility categories

-

Increased scrutiny of supplier cost submissions

-

Focus on produce and traffic-driving items

Fresh fruit deflation may allow short-term promotional support without margin erosion.

However, with food inflation at 4.8%, price sensitivity remains elevated.

2026 risk map for grocery categories

| Cost Driver | Timing | Most Exposed Categories | Retail Response |

|---|---|---|---|

| Produce harvest variability | Seasonal | Fresh fruit & vegetables | Flexible sourcing |

| Labour cost pressure | Ongoing | Bakery, prepared foods | Productivity focus |

| Currency movement | Ongoing | Imported grocery | Hedging & pricing discipline |

| Energy volatility | Variable | Ambient & frozen | Contract monitoring |

This framework is increasingly guiding supermarket buying strategies into mid-2026.

What happens next

The next CPI release will determine whether January marked the start of a sustained easing cycle or simply a temporary moderation driven by produce.

For now, the message is clear:

Canada food inflation is slowing — but it remains structurally higher than headline CPI.

For the Canada supermarket sector, that means pricing discipline, negotiation intensity and value positioning will remain central themes through the first half of 2026.

Editor’s Note: This report is based on official Consumer Price Index data released by Statistics Canada on 17 February 2026. The analysis focuses specifically on food purchased from stores and its relevance to Canada supermarket pricing, supplier negotiations and grocery category performance.