Italy grocery market is not shrinking.

But its stores are.

Across major cities and many regional hubs, the momentum in new openings is clearly moving toward smaller, neighbourhood-based formats. Instead of expanding with large out-of-town hypermarkets, retailers are focusing on compact stores embedded in daily life.

This shift is not cosmetic. It reflects a structural change in consumer behaviour, cost structures, and urban development patterns. More importantly, it redefines how suppliers must think about assortment, packaging, and logistics.

The Italian supermarket of the next decade will not necessarily be larger. It will be closer.

From Destination Retail to Daily Interception

For years, the dominant grocery model depended on the car. Consumers would drive to the outskirts, complete a large weekly shop, and fill the pantry in one trip. Assortment depth, wide aisles, bulk promotions, and parking capacity were essential parts of that system.

That pattern has weakened.

In urban areas especially, households are shopping more frequently and buying less per trip. Instead of a single large basket, many consumers now make several smaller purchases during the week. Fresh food, meal components, and immediate consumption categories are gaining importance.

Retailers are adjusting accordingly. When the shopping mission changes, store format must follow.

Large stores rely on high basket values. Smaller stores rely on frequency and repeat visits. The economic model is different.

Why Store Size Is Being Recalibrated

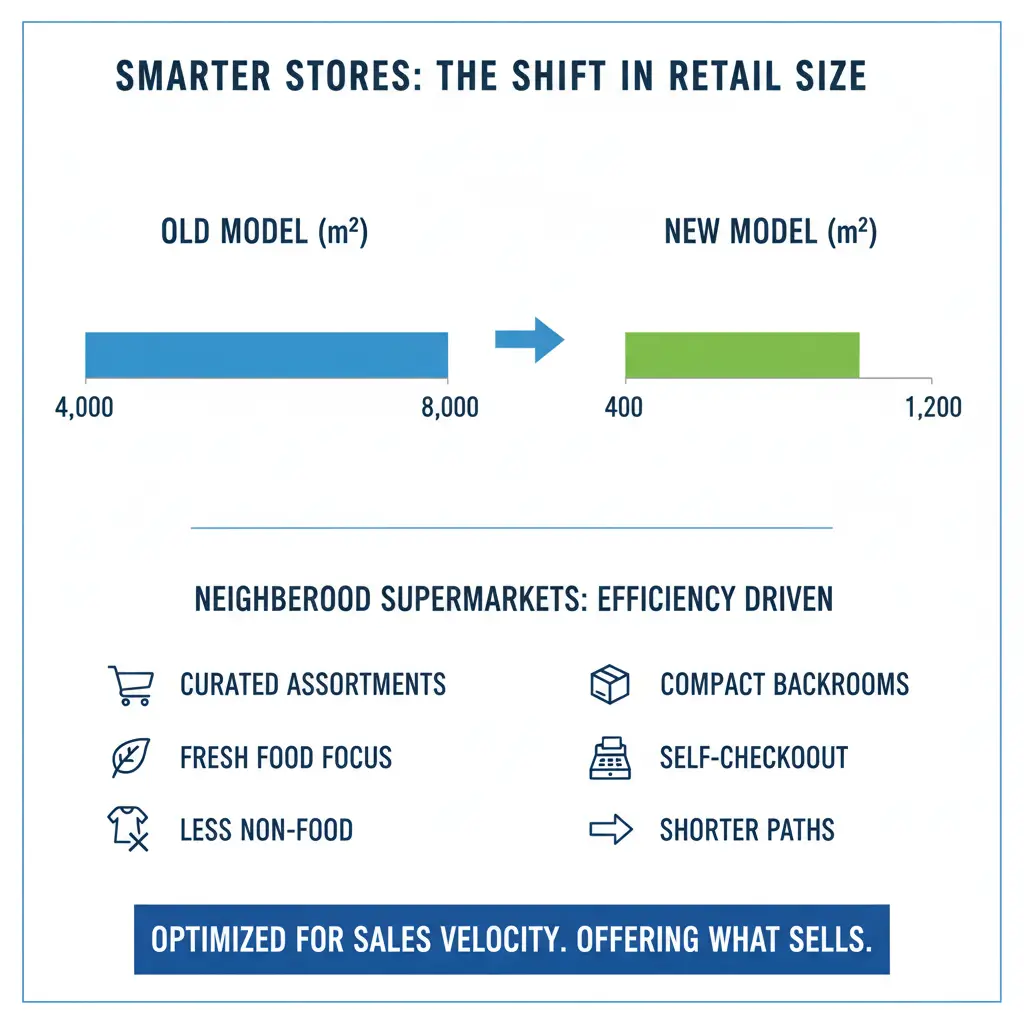

Recent openings increasingly fall in the 400–1,200 sqm range rather than 4,000–8,000 sqm developments. These are not “mini hypermarkets.” They are purpose-built neighbourhood supermarkets designed around efficiency.

Key characteristics include:

-

Curated assortments with high SKU productivity

-

Fresh-led perimeter layouts

-

Reduced non-food space

-

Compact backrooms

-

Self-checkout integration

-

Shorter customer journey paths

Every square metre must generate strong turnover. Assortment breadth is sacrificed in favour of velocity per facing.

This is not about offering less. It is about offering precisely what sells.

Urban Density Is Driving Location Strategy

Italy’s urban fabric plays a major role. Cities such as Milan, Rome, Bologna, Florence, and Turin are dense, historic, and space-constrained. Large plots suitable for hypermarkets are limited and expensive.

Retailers are increasingly targeting:

-

Ground-floor retail spaces within residential buildings

-

Units near metro and rail stations

-

High-footfall pedestrian streets

-

Mixed-use housing developments

-

Regenerated urban districts

The objective is daily interception. A store within walking distance of home can generate consistent traffic without relying on car-based destination shopping.

Proximity reduces dependency on large-scale promotional events and seasonal peaks. It builds habitual frequency.

Consumer Behaviour Is the Primary Catalyst

Format changes are reactive. They follow behaviour.

Three structural consumer shifts are shaping the Italian grocery environment.

1. Smaller Households

Italy has a significant proportion of single-person and two-person households, particularly in metropolitan regions. Smaller households purchase in lower volumes and often lack extensive storage space at home.

As a result, consumers prefer buying what they need for immediate use rather than stocking up in bulk.

2. Fresh and Meal-Based Purchasing

Proximity stores allocate more space to:

-

Fresh produce

-

Bakery

-

Dairy

-

Ready meals

-

Deli counters

-

Meal components

Ambient grocery categories remain important, but assortment depth is narrower. Frozen sections are more compact. Non-food ranges are limited to essentials.

Fresh rotation becomes central to profitability.

3. Time Efficiency

Price sensitivity remains present in Italy, but convenience is gaining weight. Consumers value shorter queues, intuitive layouts, and speed of purchase.

Smaller stores enable easier navigation and faster checkout. For time-pressed urban households, that efficiency matters.

The mission is increasingly about quick solutions, not extended browsing.

Basket Size and Frequency Dynamics

Average basket values in neighbourhood formats are typically lower than in traditional hypermarkets. However, visit frequency compensates for smaller transaction sizes.

Retailers are optimising for:

-

10–20 item baskets

-

Daily meal purchases

-

Top-up missions

-

Immediate consumption

This has structural consequences. Promotion mechanics change. Bulk discount strategies lose some effectiveness. Private label positioning must adapt to smaller basket logic.

Impulse zones and meal-solution bundles become more relevant.

Urban Versus Regional Patterns

The transition toward compact formats is most visible in northern and central urban regions, where population density and real estate constraints support neighbourhood retail.

In southern and rural provinces, mid-sized supermarkets remain relevant due to car dependency and different housing patterns. However, even in these regions, new openings are often smaller than those built fifteen years ago.

Retailers are limiting capital exposure per site. Smaller footprints reduce risk and allow faster rollout.

The model is becoming more adaptable and location-specific.

Cost Structure Is Influencing Strategic Decisions

Operating a large-format store requires:

-

Higher energy consumption

-

Larger refrigeration loads

-

Greater staffing

-

Deeper inventory commitments

-

Longer construction timelines

Compact stores offer operational advantages:

-

Lower utility intensity

-

Reduced labour exposure

-

Faster time-to-market

-

Leaner stock holding

-

Lower real estate risk

Energy volatility and inflationary pressures have reinforced the appeal of flexible formats. Smaller stores are easier to optimise operationally and financially.

Retailers are prioritising agility over scale.

The Rise of Hybrid Convenience-Supermarket Models

Italy is not moving toward pure convenience retail in the traditional sense. Instead, it is developing hybrid neighbourhood supermarkets that combine depth and speed.

Many compact stores now integrate:

-

Fresh counters

-

Ready-meal sections

-

Coffee corners

-

Digital loyalty systems

-

Self-checkout lanes

-

Click-and-collect options

These features reflect daily rhythms: morning commuters, lunchtime buyers, after-work fresh purchases, and weekend top-ups.

The store is becoming part of routine, not a destination event.

What Formats Are Performing Best?

Resilient small-format stores share several attributes:

-

400–1,200 sqm footprint

-

Strong fresh perimeter

-

High private label penetration

-

Focused SKU count

-

Clear signage and easy navigation

-

Integrated digital payment systems

Turnover per sqm becomes the primary performance metric. Shelf productivity replaces assortment breadth as the central KPI.

Retailers are trading variety for efficiency.

Implications for Assortment Strategy

Compact formats cannot carry hypermarket-level SKU counts. Assortment compression is inevitable.

Suppliers face higher performance thresholds. Each SKU must demonstrate strong rotation and differentiation.

Low-velocity variants are increasingly vulnerable to delisting.

Category managers must prioritise:

-

Clear price architecture

-

High-volume SKUs

-

Strong brand recognition

-

Efficient shelf utilisation

Innovation cycles may shorten, but only products with clear velocity potential will secure space.

Packaging and Case-Pack Considerations

Neighbourhood formats create operational constraints:

-

Limited shelf depth

-

Smaller backrooms

-

Frequent replenishment

-

Urban delivery limitations

Suppliers must consider:

-

Shelf-ready packaging

-

Smaller case-pack configurations

-

Stackable secondary formats

-

Efficient palletisation for mixed loads

Packaging designed for large display pallets may not align with compact-store logistics.

Operational compatibility becomes a competitive advantage.

Logistics and Delivery Flexibility

Smaller stores often require:

-

More frequent deliveries

-

Smaller drop sizes

-

Higher forecasting accuracy

-

Tight inventory management

Urban delivery networks can be complex. Access restrictions and limited unloading space add operational challenges.

Suppliers capable of supporting flexible distribution models gain leverage in negotiations.

Logistics precision becomes as important as pricing.

The Strategic Role of Private Label

Private label plays a central role in compact formats. Limited assortment favours products that provide margin control and brand loyalty.

Retailers prioritise private label SKUs that:

-

Deliver consistent turnover

-

Align with fresh-led positioning

-

Fit smaller basket logic

-

Reinforce value perception

National brands must compete for tighter shelf space. Clear differentiation and marketing support become essential.

Local Sourcing and Neighbourhood Identity

Compact stores often emphasise regional identity. Highlighting local producers strengthens neighbourhood positioning.

Shorter supply chains also align with sustainability narratives and freshness expectations.

For regional suppliers, small-format expansion may create entry opportunities that were previously difficult within hypermarket-dominated assortments.

Local alignment can become a gateway strategy.

Why Italy’s Supermarkets Are Shrinking to Grow

The recalibration toward smaller formats reflects multiple converging factors:

-

Urban density and real estate constraints

-

Smaller household structures

-

Higher shopping frequency

-

Fresh-led consumption patterns

-

Energy and cost pressures

-

Demand for convenience

This is not a temporary adjustment. It represents a structural evolution in how grocery retail operates.

Retailers are optimising for flexibility, speed, and local proximity rather than scale alone.

Supplier Action Framework

Below is a consolidated summary of how the format shift translates into supplier strategy.

| Retail Shift | Operational Impact | Supplier Action |

|---|---|---|

| Smaller footprints | Reduced shelf capacity | Prioritise high-rotation SKUs |

| Higher frequency shopping | More replenishment cycles | Support flexible drop volumes |

| Fresh-led layouts | Perimeter emphasis | Align portfolio with meal solutions |

| Curated assortments | SKU rationalisation | Focus on core variants |

| Urban delivery complexity | Smaller load sizes | Optimise case packs and pallet mixes |

| Hybrid convenience models | Mixed missions | Adapt packaging for small baskets |

The Long-Term Outlook

Italy’s grocery sector is not abandoning larger stores entirely. Hypermarkets will remain part of the landscape, particularly in suburban areas.

However, incremental expansion is clearly favouring compact neighbourhood formats.

This shift influences:

-

Capital allocation

-

Category planning

-

Packaging development

-

Distribution design

-

Procurement negotiations

Suppliers aligned with hypermarket logic alone risk strategic misalignment.

The competitive battleground is no longer only price per unit or promotional scale. It is relevance per square metre.

Italy’s supermarkets are reducing physical size, but expanding presence within everyday routines.

In today’s grocery environment, proximity is not just convenience.

It is strategy.