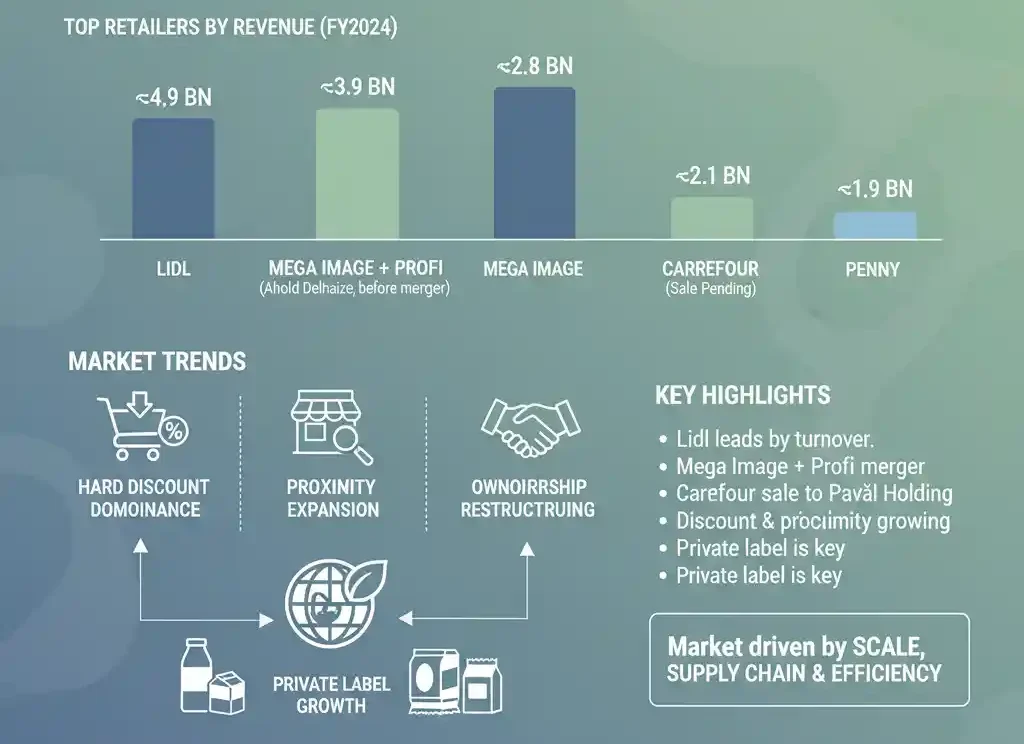

Romania grocery retail market in 2026 is led by Lidl Romania, followed by Kaufland Romania and the newly consolidated Mega Image–Profi group under Ahold Delhaize. Based on FY2024 financial reporting, the sector is defined by hard discount dominance, proximity expansion, and major ownership restructuring including Carrefour’s proposed sale to Pavăl Holding.

As of FY2024 reporting, Lidl Romania is the largest supermarket chain in Romania by revenue, generating approximately 24.6 billion RON in turnover, ahead of Kaufland Romania and the combined Mega Image–Profi network under Ahold Delhaize.

Romania modern grocery retail market is concentrated but highly competitive. The top three operators control a substantial share of total FMCG retail turnover, with discount and proximity formats expanding faster than traditional hypermarkets.

Hard discount chains now account for a growing share of national grocery spending, while hypermarkets remain relevant for high basket value and non-food rotation.

Revenue Ranking – Largest Supermarket Chains in Romania (FY2024)

| Rank | Retailer | FY2024 Revenue (RON) | Approx. € Equivalent* | Parent Group | Core Format |

|---|---|---|---|---|---|

| 1 | Lidl Romania | ~24.6 bn | ~€4.9 bn | Schwarz Group | Hard Discount |

| 2 | Kaufland Romania | ~19.6 bn | ~€3.9 bn | Schwarz Group | Hypermarket |

| 3 | Profi | ~14.1 bn | ~€2.8 bn | Ahold Delhaize | Proximity |

| 4 | Carrefour Romania | ~12.5 bn | ~€2.5 bn | Sale to Pavăl Holding (pending) | Multi-format |

| 5 | Mega Image | ~10.6 bn | ~€2.1 bn | Ahold Delhaize | Urban Supermarket |

| 6 | Penny Romania | ~9.4 bn | ~€1.9 bn | REWE Group | Discount |

| 7 | Auchan Romania | ~7.7 bn | ~€1.5 bn | Auchan Group | Hyper + Proximity |

| 8 | Metro Romania | ~6.5+ bn | ~€1.3 bn | Metro AG | Cash & Carry |

| 9 | Selgros Romania | ~4.5 bn | ~€0.9 bn | Transgourmet | Cash & Carry |

| 10 | Annabella | ~1+ bn | ~€0.2 bn | Romanian-owned | Regional Supermarket |

*Currency reference approx. 1 EUR = 5 RON (average rate).

1. Lidl Romania

Lidl Romania is the largest supermarket chain in Romania by revenue in 2026.

Part of Germany’s Schwarz Group, Lidl entered Romania in 2011 and rapidly expanded through an aggressive discount model. By FY2024, turnover reached approximately 24.6 billion RON.

Core Categories

-

Packaged FMCG

-

Fresh produce

-

Private label dairy and ambient goods

-

Weekly promotional non-food items

Lidl’s operational model relies heavily on private label penetration, lean store operations, and centralised logistics. Its ability to maintain price perception leadership while expanding footprint has allowed it to surpass Kaufland in turnover.

Private label brands form a structural margin engine. High SKU discipline reduces complexity while maintaining turnover velocity.

2. Kaufland Romania

Kaufland remains Romania’s largest hypermarket operator and second-largest grocery retailer.

Also owned by Schwarz Group, Kaufland generated approximately 19.6 billion RON in FY2024.

Founded in Germany in 1984 and entering Romania in 2005, Kaufland operates large-format stores that combine food retail with non-food assortments.

Core Categories

-

Fresh meat and produce

-

Household FMCG

-

Non-food seasonal promotions

-

Private label portfolio

Kaufland’s strength lies in store productivity per location. While discount operators focus on limited assortment, Kaufland retains high basket size and broader category depth.

3. Profi (Ahold Delhaize Integration)

Profi is Romania’s largest proximity supermarket network by store count.

Founded in Belgium in 1979 and expanding into Romania in the late 1990s, Profi reported approximately 14.1 billion RON in FY2024.

In 2024–2025, Ahold Delhaize completed the acquisition of Profi, integrating it with Mega Image operations.

Core Categories

-

Neighbourhood grocery

-

Fresh daily essentials

-

Private label staples

-

Urban convenience retail

Profi’s value lies in density. With thousands of stores across small towns and regional areas, the chain dominates frequent-basket purchasing behaviour.

4. Carrefour Romania

Carrefour Romania is the fourth-largest supermarket chain in Romania by revenue in 2026.

Part of France’s Carrefour Group, the company entered Romania in 2001 and expanded nationally through a multi-format retail model. By FY2024, turnover reached approximately 12.5 billion RON.

Core Categories

- Fresh food and produce

- Packaged FMCG

- Private label grocery

- Hypermarket non-food assortments

Carrefour operates hypermarkets, supermarkets, and convenience formats, giving it one of the most diversified store portfolios in the Romanian market. The full integration and rebranding of Cora Romania strengthened its national footprint, with Cora no longer operating as a separate brand.

Carrefour’s operational model combines large-format basket retail with proximity coverage in urban areas. However, in 2026 the company entered exclusive negotiations to sell its Romanian operations to Pavăl Holding, marking a potential ownership transition subject to regulatory approval.

5. Mega Image

Mega Image is Romania’s dominant urban supermarket chain.

Part of Ahold Delhaize, Mega Image generated approximately 10.6 billion RON in FY2024.

Founded in Belgium in 1995 and entering Romania in 2000, the chain focuses on urban density and proximity formats.

Core Categories

-

Fresh food

-

Premium private label

-

Urban grocery assortments

The integration with Profi creates a combined entity that rivals Lidl in scale.

6. Penny Romania

Penny is Romania’s fastest-growing pure discount competitor after Lidl.

Owned by Germany’s REWE Group, Penny reached approximately 9.4 billion RON in FY2024.

Core Categories

-

Discount FMCG

-

Fresh meat

-

Private label food

-

Promotional weekly offers

Penny continues expansion into secondary cities and regional towns.

7. Auchan Romania

Auchan Romania is the seventh-largest supermarket chain in Romania by revenue in 2026.

Part of France’s Auchan Group, the company entered Romania in 2006 and expanded through large-format hypermarkets. By FY2024, turnover reached approximately 7.7 billion RON.

Core Categories

- Fresh food and produce

- Packaged FMCG

- Non-food seasonal assortments

- Private label grocery

Auchan operates hypermarkets alongside MyAuchan smaller urban formats, allowing it to compete across both large basket and proximity segments. The brand maintains strong presence in major cities while adapting to format diversification.

Facing sustained pressure from hard discount operators, Auchan is optimising store formats, reducing hypermarket dependency, and strengthening smaller-format expansion to maintain competitiveness in a price-driven environment.

8. Metro Romania

Metro operates primarily in wholesale and Horeca supply.

Revenue exceeded 6.5 billion RON.

Founded in Germany in 1964, Metro serves professional customers and supports franchise networks including La Doi Pași.

Its role is structurally important for supply chain integration rather than consumer retail dominance.

9. Selgros Romania

Selgros Romania is the ninth-largest food retail operator in Romania by revenue in 2026, operating in the cash & carry wholesale segment.

Owned by Transgourmet Holding, Selgros entered Romania in 2001 and developed a national wholesale footprint serving both professional and retail customers. By FY2024, revenue reached approximately 4.5 billion RON.

Core Categories

- Bulk grocery and FMCG

- Fresh meat and produce

- Horeca supply

- Private label wholesale assortments

Selgros operates large-format cash & carry stores designed for professional clients, independent retailers, and foodservice operators. Its model differs from traditional supermarkets, focusing on volume sales and business customers rather than household basket retail.

In 2026, Selgros continues to maintain a stable position within Romania’s wholesale food distribution segment, with emphasis on Horeca recovery and supply chain efficiency.

10. Annabella

Annabella is the largest fully Romanian-owned supermarket chain by revenue in 2026.

Founded in Romania in 1994, Annabella developed as a regional retail operator before expanding its footprint through acquisitions and store network growth. By FY2024, revenue surpassed 1 billion RON.

Core Categories

- Fresh food and produce

- Packaged FMCG

- Private label staples

- Regional grocery assortments

Annabella operates supermarket-format stores concentrated in regional markets, with a focus on neighbourhood accessibility and local sourcing. The chain strengthened its position following the acquisition of divested stores from the Ahold Delhaize integration process.

In 2026, Annabella continues expanding its regional footprint while reinforcing its position as the most significant domestically owned supermarket chain in Romania.

Market Structure Analysis

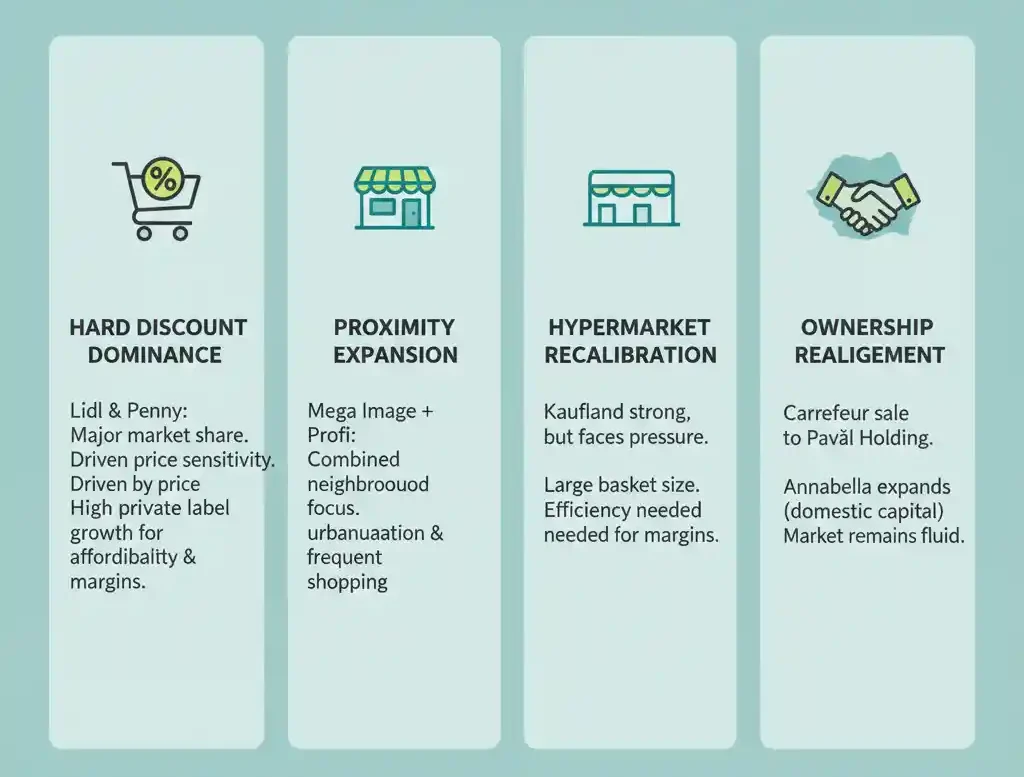

Hard Discount Dominance

Lidl and Penny together represent a major share of modern grocery spending.

Price sensitivity remains a defining consumer behaviour driver. High private label penetration improves margin resilience while maintaining affordability.

Proximity Expansion

Mega Image and Profi’s combined footprint signals a shift toward neighbourhood formats.

Urbanisation, traffic density, and frequency-based shopping behaviour favour smaller stores with daily essentials.

Hypermarket Recalibration

Kaufland remains strong, but hypermarkets face structural pressure from discount and proximity formats.

Large basket size supports revenue, but margin compression and operating costs require efficiency optimisation.

Ownership Realignment

Carrefour’s proposed sale to Pavăl Holding and Annabella’s expansion reflect increasing domestic capital presence in Romanian retail.

The market remains internationally dominated but structurally fluid.

Private Label as A Structural Driver

Private label growth is a defining factor in 2026.

Operators including Lidl, Kaufland, Carrefour, and Mega Image continue expanding proprietary brands across:

-

Dairy

-

Ambient grocery

-

Frozen products

-

Household goods

Private label penetration supports gross margin improvement and competitive price positioning.

Industry Outlook 2026–2027

Romania’s grocery sector is expected to continue:

-

Discount expansion

-

Proximity consolidation

-

Private label growth

-

Operational efficiency investments

-

Strategic ownership transitions

Revenue leadership is likely to remain concentrated among Lidl, Kaufland, and the integrated Ahold Delhaize network.

Conclusion

The largest supermarket chains in Romania are led by Lidl Romania, followed by Kaufland and the integrated Mega Image–Profi group. Hard discount dominance, proximity expansion, and ownership restructuring define the competitive landscape entering 2026.

These shifts will continue shaping A brands in Romania, influencing supplier negotiations and private label strategies, while also driving new investment in packaging in Romania across fresh, ambient, and FMCG categories.

Romania’s grocery market has moved from rapid expansion to structural consolidation, with scale, supply chain control, and operational efficiency determining long-term leadership.

Editor’s Note: This article is based exclusively on publicly available FY2024 financial disclosures, corporate reports, and regulatory filings. Currency conversions are approximate based on average exchange rates. No speculative data has been used.