Greece’s packaging manufacturing sector has entered a new consolidation phase. Over the past two years, producers have expanded capacity, upgraded production lines, and aligned operations more tightly with supermarket private label supply chains across Southern and Central Europe. At the same time, structural shifts — including the exit of domestic glass container production — have reshaped how packaging is sourced and supplied into the Greek market.

This ranking of Packaging Companies in Greece reflects verified manufacturing activity, revenue scale, and operational relevance for FMCG and retail supply chains. Only companies with active production footprints inside Greece are included. Financial figures are based on publicly available FY2024–FY2025 company disclosures and registry filings.

10 Packaging Companies in Greece — Revenue and Manufacturing Focus

| Rank | Company | Latest Revenue | Fiscal Period | Main Packaging Categories | Estimated Workforce |

|---|---|---|---|---|---|

| 1 | Plastika Kritis Group | €385m+ | FY2024 | Stretch film, industrial film, flexible materials | 2,000+ |

| 2 | Thrace Group (Thrace Plastics) | €385m–€390m | FY2025 | PP woven packaging, industrial packaging materials | 1,900+ |

| 3 | Crown Hellas Can Packaging | €185m | FY2024 | Aluminium beverage cans | 500+ |

| 4 | Flexopack S.A. | €170m+ | FY2025 (TTM) | Flexible food packaging films, laminates | 600+ |

| 5 | A. Hatzopoulos S.A. | €113m | FY2024 | Flexible packaging, printed films | 500+ |

| 6 | ADAPA Greece Komotini | €83m | FY2024 | Flexible packaging conversion | 300+ |

| 7 | Dunapack Packaging Hellas | €63m | FY2024 | Corrugated packaging | 350+ |

| 8 | Daios Plastics | €55m | FY2024 | Flexible packaging films, laminates | 300+ |

| 9 | Unipakhellas Central | €53m | FY2024 | Paper-based packaging, labels | 300+ |

| 10 | Matrix Pack S.A. | €39m | FY2024 | Molded fibre packaging | 200+ |

Revenues rounded for clarity. Workforce ranges reflect publicly disclosed employment data and industry filings.

Sustainability and Compliance Positioning

| Company | Core Sustainability Focus | Common Certifications / Frameworks | Operational Relevance |

|---|---|---|---|

| Plastika Kritis | Certified circular polymers, recycled feedstocks | ISCC PLUS, ISO systems | Supports mass-balance materials and recycled content programs |

| Thrace Group | Material efficiency, industrial recycling | ISO 14001, ESG frameworks | Export packaging compliance |

| Crown Hellas | Lightweight metal packaging, energy efficiency | Beverage packaging standards | High-speed beverage line compatibility |

| Flexopack | Food safety packaging controls | BRCGS Packaging, ISO 9001 | Required for large FMCG supply chains |

| Hatzopoulos | Paper traceability, environmental management | FSC CoC, ISO 14001 | Retail packaging compliance |

| ADAPA Greece | Group sustainability systems | ISO quality and environment frameworks | Multi-country packaging alignment |

| Dunapack Hellas | Recycled fibre sourcing | FSC CoC (group) | Retail logistics packaging |

| Daios Plastics | Film downgauging, recyclability projects | ISO systems | Cost-efficient flexible packaging |

| Unipakhellas | Responsible paper sourcing | ISO quality frameworks | Label and paper packaging compliance |

| Matrix Pack | Fibre substitution, plastic reduction | CSR frameworks | Plastic replacement projects |

Company Profiles

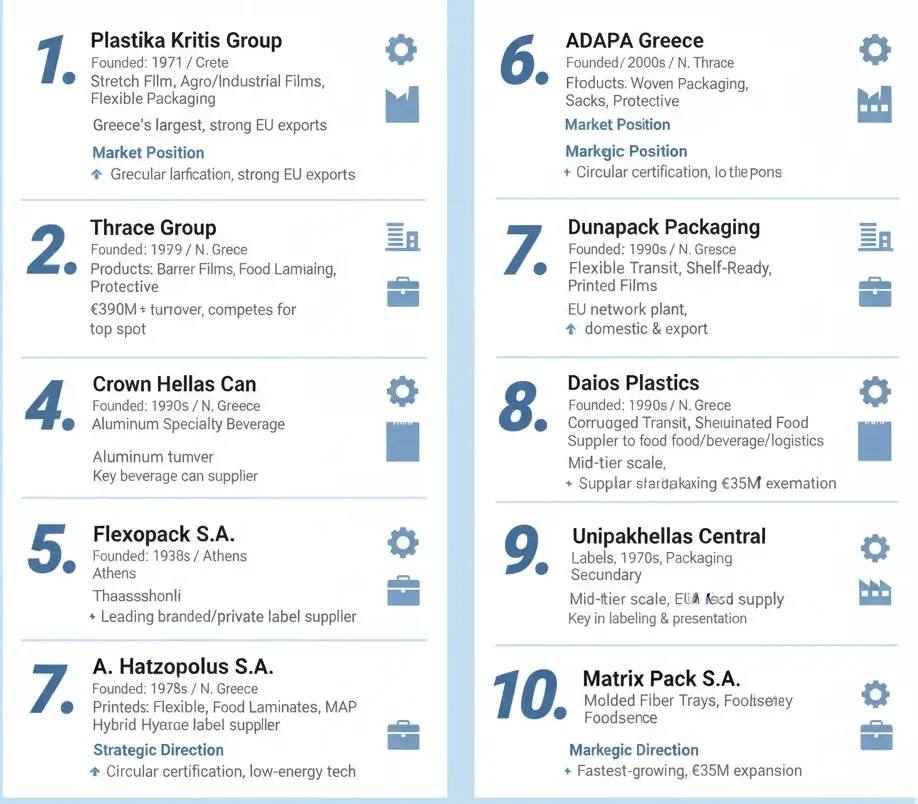

1. Plastika Kritis Group

Founded: 1971

Origin: Heraklion, Crete

Core product categories:

-

Stretch film and pallet wrap

-

Industrial and agricultural films

-

Flexible packaging materials

Market position and scale

Plastika Kritis remains Greece’s largest polymer-based packaging manufacturer by turnover. Its production network supports domestic FMCG distribution while maintaining strong export volumes into Western and Central Europe. The group operates high-output extrusion and converting lines and has continued to modernise automation and quality inspection systems.

Operational relevance

For supermarket logistics, stretch film performance directly affects pallet stability, warehouse efficiency, and transport damage rates. Plastika Kritis plays a central role in secondary packaging supply for large distribution networks.

Strategic direction

The company is expanding circular material certification coverage and investing in lower-energy production technologies.

2. Thrace Group (Thrace Plastics)

Founded: 1979

Origin: Northern Greece industrial zone

Core product categories:

-

Woven packaging materials

-

Industrial sacks and bulk packaging

-

Protective packaging solutions

Market position and scale

By late 2025, Thrace Group reached turnover levels approaching €390 million, placing it in direct competition with Plastika Kritis for the top market position. The group operates across multiple industrial material categories with strong export penetration.

Operational relevance

Thrace supplies packaging materials used across upstream FMCG supply chains, including bulk ingredient transport and industrial logistics linked to supermarket production ecosystems.

Strategic direction

Investment continues into advanced material engineering and operational efficiency upgrades.

3. Crown Hellas Can Packaging

Founded: 1990s (Greek operations)

Origin: Part of Crown Holdings global network

Core product categories:

-

Aluminium beverage cans

-

Specialty beverage packaging formats

Market position and scale

Crown Hellas operates one of the country’s most important beverage can production facilities. Output volumes serve both multinational beverage bottlers and private label drink producers.

Operational relevance

Can quality consistency affects filling line performance, seal integrity, and shelf appearance. This makes Crown Hellas operationally critical for private label beverage programs.

Strategic direction

The company continues to invest in lightweight can technology and energy efficiency improvements.

4. Flexopack S.A.

Founded: 1978

Origin: Athens industrial region

Core product categories:

-

Barrier packaging films

-

Food packaging laminates

-

Modified atmosphere packaging solutions

Market position and scale

By late 2025, Flexopack’s trailing twelve-month revenue exceeded €170 million, reflecting strong export demand and increased flexible packaging consumption across food categories.

Operational relevance

Flexopack’s packaging structures directly impact shelf life, food safety, and chilled product distribution. Its materials are widely used across meat, dairy, bakery, and ready-meal segments.

Strategic direction

The company is accelerating development of recyclable mono-material structures and downgauged film formats.

5. A. Hatzopoulos S.A.

Founded: 1931

Origin: Thessaloniki

Core product categories:

-

Printed flexible packaging

-

Food-grade laminates

-

Hybrid paper-plastic packaging

Market position and scale

Hatzopoulos combines legacy printing expertise with modern converting infrastructure. It remains one of Greece’s strongest suppliers for branded and private label flexible packaging.

Operational relevance

Artwork accuracy, print consistency, and traceability systems are critical for supermarket private label compliance. Hatzopoulos maintains strong quality control frameworks that support this requirement.

Strategic direction

The company continues expanding recyclable packaging capacity and FSC-certified material coverage.

6. ADAPA Greece Komotini

Founded: 2000s

Origin: Thrace region

Core product categories:

-

Flexible food packaging

-

Printed packaging films

Market position and scale

As part of a European flexible packaging network, ADAPA Greece operates a strategically positioned conversion plant serving both domestic and export customers.

Operational relevance

Network integration allows flexible volume balancing and supply continuity across multiple production locations.

Strategic direction

Focus remains on packaging standardisation and mono-material product development.

7. Dunapack Packaging Hellas

Founded: 1990s

Origin: Central Greece

Core product categories:

-

Corrugated transit packaging

-

Shelf-ready retail packaging

-

Distribution cases

Market position and scale

Dunapack Hellas supplies corrugated packaging to food producers, beverage bottlers, and logistics operators serving supermarket distribution centres.

Operational relevance

Corrugated packaging performance affects warehouse throughput, shelf replenishment speed, and transport efficiency.

Strategic direction

The company continues to increase recycled fibre usage and lightweight board development.

8. Daios Plastics

Founded: 1980s

Origin: Northern Greece

Core product categories:

-

Flexible packaging films

-

Laminated food packaging

Market position and scale

Daios Plastics operates active production lines serving domestic FMCG customers and export markets. The company maintains stable mid-tier manufacturing scale.

Operational relevance

Daios supports flexible packaging supply for food producers supplying private label programs across Southern Europe.

Strategic direction

Investment remains focused on film performance optimisation and production efficiency.

9. Unipakhellas Central

Founded: 1970s

Origin: Athens region

Core product categories:

-

Labels and printed materials

-

Paper-based packaging

-

Secondary packaging solutions

Market position and scale

Unipakhellas Central plays a key role in packaging presentation and regulatory labeling across FMCG categories.

Operational relevance

Accurate labeling is essential for supermarket compliance, barcode scanning reliability, and product traceability.

Strategic direction

Digital printing and short-run packaging capabilities continue to expand.

10. Matrix Pack S.A.

Founded: 2009

Origin: Northern Greece

Core product categories:

-

Molded fibre trays and containers

-

Foodservice and retail packaging

Market position and scale

Matrix Pack has become one of Greece’s fastest-growing fibre packaging manufacturers. In late 2025, the company completed a €35 million production expansion, significantly increasing output capacity.

Operational relevance

Fibre packaging is increasingly adopted in private label ready meals, fresh food trays, and takeaway packaging.

Strategic direction

Product development now focuses on moisture resistance, heat tolerance, and improved stacking performance.

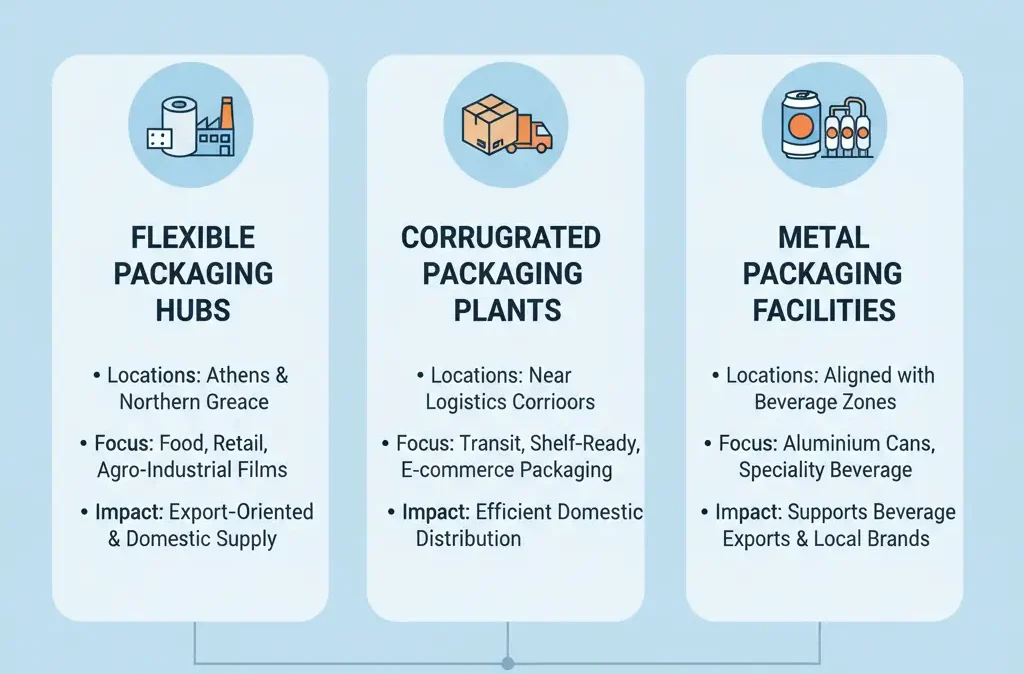

Market Structure Impact

Greek packaging manufacturing is organised around three main industrial clusters:

-

Flexible packaging hubs in Athens and Northern Greece

-

Corrugated packaging plants positioned near logistics corridors

-

Metal packaging facilities aligned with beverage production zones

This structure supports export logistics while maintaining efficient domestic distribution coverage.

Category Dominance Trends

Flexible packaging leadership

Flexible packaging continues to dominate investment activity. Food exports, chilled product growth, and private label expansion are driving sustained demand.

Beverage packaging stability

Metal can production remains closely linked to tourism growth and beverage private label expansion.

Fibre packaging acceleration

Molded fibre adoption is rising as supermarkets reduce plastic usage in selected product categories.

Note on Glass Packaging in Greece

Following the permanent closure of BA Glass’s Egaleo factory in 2024/2025, Greece no longer operates domestic glass container manufacturing facilities. All commercial glass packaging used by Greek beverage producers and FMCG manufacturers is now imported, primarily from plants in Bulgaria and Romania.

This structural change has affected lead times, logistics planning, and supply chain resilience for glass-dependent product categories.

Industry Direction

Investment priorities across Greek packaging manufacturing now centre on:

-

Automation and robotics

-

Energy efficiency upgrades

-

Certified recycled material sourcing

-

Lightweight packaging engineering

-

Digital traceability integration

Smaller converters increasingly partner with larger groups to maintain compliance and export competitiveness.

Structural Change Outlook

Consolidation pressure is expected to increase through 2026–2028. Larger manufacturers with strong export pipelines and capital access will continue gaining share. Smaller producers are likely to specialise in niche formats such as short-run packaging, foodservice solutions, and specialty printing.

At the same time, supermarket private label growth across Southern Europe is expected to stabilise packaging demand volumes and encourage long-term supplier partnerships.

Conclusion

The Greek packaging manufacturing sector has transitioned into a mature export-oriented production base. Investment in flexible packaging, metal containers, corrugated logistics materials, and fibre alternatives continues to reshape industrial capacity.

For Greek FMCG and supermarket supply chains, Packaging Companies in Greece now offer a combination of production scale, compliance maturity, and export readiness. The next growth phase will be shaped by sustainability regulation, private label expansion, and continued operational consolidation.

Editor’s Note: All financial and operational information in this article is based on publicly available company financial reports, regulatory filings, and verified business registry disclosures for FY2024–FY2025. No private estimates or unverified figures were used.