Romanian-owned private label manufacturers supply major supermarket chains including Kaufland, Carrefour, Lidl, Auchan, Profi and Mega Image. In 2026, the largest domestic food producers combine billion-RON turnover, integrated production systems and certified food safety compliance to support supermarket own-brand growth across poultry, processed meat, pasta and staples.

A private label manufacturer produces food products that are sold under a supermarket’s own brand rather than the producer’s brand. In Romania, these companies manufacture poultry, processed meat, pasta, flour, frozen goods and beverages that appear on supermarket shelves under retailer labels.

Top Romanian Private Label Manufacturers (FY2024)

| Rank |

Company |

FY2024 Revenue (RON) |

Core Category |

Ownership |

| 1 |

Cris-Tim |

1.12 Billion |

Processed Meat |

Romanian |

| 2 |

Agricola International |

1.21 Billion (Group) |

Poultry |

Romanian |

| 3 |

Transavia |

~1 Billion (Group) |

Poultry |

Romanian |

| 4 |

Unicarm |

~438 Million |

Meat Processing |

Romanian |

| 5 |

Pambac |

~290 Million |

Pasta & Milling |

Romanian |

| 6 |

Boromir Group |

Industrial Scale |

Milling & Bakery |

Romanian |

| 7 |

Safir |

Industrial Scale |

Poultry |

Romanian |

| 8 |

Macromex |

Industrial Scale |

Frozen Foods |

Romanian |

| 9 |

Zarea |

Industrial Scale |

Wine |

Romanian |

| 10 |

Sam Mills |

Export-Oriented Scale |

Pasta & Corn Products |

Romanian |

Revenue figures reflect 2024/2025 public disclosures and business reporting. Where consolidated figures apply, group revenue is used.

How are the top Romanian private label manufacturers ranked?

Private label manufacturing in Romania is defined by four key requirements:

-

Romanian majority ownership

-

FY2024 revenue scale consistent with national supermarket supply

-

Industrial production capacity in Romania

-

Compliance with international food safety standards (IFS, BRCGS, ISO 22000, HACCP)

Revenue is the primary ranking factor. Production integration and private label exposure determine placement.

Who are the top 10 Romanian-owned food manufacturers in 2026?

Below is the verified ranking based on updated financial indicators.

1. Cris-Tim Family Holding

FY2024 Revenue: 1.12 Billion RON

Category: Processed meat, chilled foods

Ownership: Romanian entrepreneurial group

Cris-Tim operates large-scale industrial meat processing facilities and has transitioned to a holding structure, reflecting its corporate expansion and operational scale. In 2025, its private label production grew by approximately 8% year on year, strengthening its position as a key supplier for supermarket own-brand programs.

The company serves as a high-volume processed meat partner for retailer cold-cut ranges and maintains multi-chain presence within the chilled category across modern retail networks.

2. Agricola International

FY2024 Group Revenue: 1.21 Billion RON

Category: Poultry and prepared foods

Ownership: Romanian

Agricola operates a vertically integrated poultry chain that covers feed production, farming, slaughtering and processing, giving it full control over the supply cycle. With consolidated revenue exceeding 1.2 billion RON, it ranks among Romania’s largest domestic food producers. Its integrated structure enables consistent high-volume delivery under retailer brands, positioning the company as a national protein supply anchor within modern supermarket networks.

3. Transavia

FY2024 Group Revenue: Approximately 1 Billion RON

Category: Poultry

Ownership: 100% Romanian family-owned

Transavia operates fully integrated poultry facilities, managing the entire production chain from farming to processing. With output exceeding 120,000 tonnes annually and revenue around the one-billion-RON level, it stands among Romania’s dominant protein producers. Its vertically controlled structure makes it well suited for high-volume supermarket private label contracts, reinforcing its position as a national leader in poultry supply within modern retail.

4. Unicarm

FY2024 Revenue: Approximately 438 Million RON

Employees: ~1,100

Category: Meat processing

Ownership: Romanian

Unicarm combines integrated meat processing operations with established retail distribution depth, particularly across regional markets. Its strong regional presence and substantial workforce provide the operational capacity required for private label production in chilled and processed meat categories. This structure allows the company to act as a flexible, regional-scale supplier and a dependable supermarket partner within its core operating areas.

5. Pambac

FY2024 Revenue: Approximately 290 Million RON

Category: Pasta and milling

Ownership: Romanian

Pambac, headquartered in Bacău, is a significant Romanian producer of pasta and flour, operating at industrial scale within the staple foods segment. Pasta continues to represent a core private label category in Romania, supported by steady household consumption and price-sensitive demand. Pambac’s high-volume manufacturing capacity enables it to supply supermarket own-brand pasta and flour ranges, reinforcing its role as a staple goods supplier within modern retail networks.

6. Boromir Group

FY2024 Revenue: Industrial-scale national producer (exact figure requires consolidated extraction)

Category: Milling and bakery

Boromir operates flour mills and bakery production units across Romania, giving it a strong industrial base in staple food manufacturing. Milling remains foundational for private label flour and bakery products, particularly in high-volume and seasonal categories. Through its production network, Boromir serves as a key partner for supermarket flour and bakery ranges and maintains a national presence within the staple goods supply chain.

7. Safir

Category: Poultry

Ownership: Romanian

Safir operates poultry slaughtering and processing facilities at industrial scale, positioning the company within Romania’s structured protein supply segment. In private label manufacturing, production volume and processing capacity are decisive factors for eligibility, and Safir meets the operational threshold required by modern retail chains. This enables the company to function as a supplementary poultry supplier within supermarket private label programs.

8. Macromex

Category: Frozen foods

Ownership: Romanian

Macromex operates in frozen food production and distribution, a segment that depends heavily on cold-chain infrastructure and coordinated industrial logistics. Frozen private label programs require reliable storage, transport and supply continuity, areas where Macromex maintains operational capability. This positions the company as a structured frozen private label partner across supermarket freezer categories.

9. Zarea

Category: Wine and sparkling wine

Ownership: Romanian

Zarea is a long-standing Romanian wine producer with established industrial bottling capability and national distribution reach. Its production infrastructure supports custom-branded wine lines tailored to retailer specifications, allowing the company to participate in supermarket private label programs within the wine and sparkling wine segment.

10. Sam Mills

Category: Pasta and corn-based products

Ownership: Romanian

Sam Mills operates export-oriented pasta and grain processing facilities, with industrial capacity in corn- and wheat-based products. Its production scale and processing specialization allow it to manufacture grain-based items that align with supermarket private label requirements, particularly in staple and value-focused retail segments.

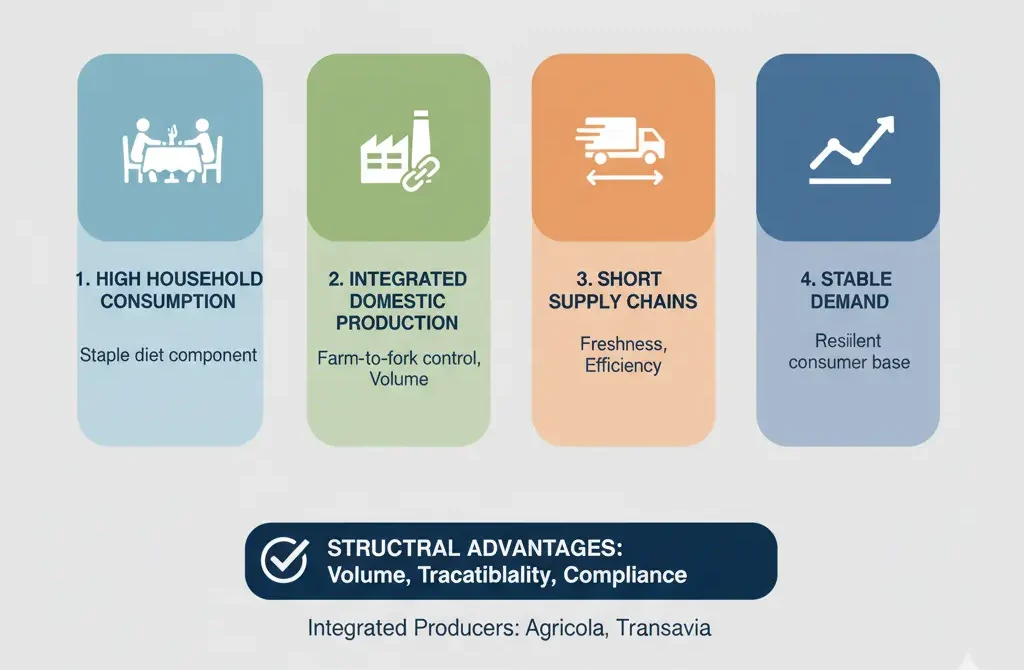

Why Does Protein Dominate Romanian Private label Manufacturing?

Poultry and processed meat represent the largest private label segments due to:

Integrated protein producers such as Agricola and Transavia have structural advantages in volume, traceability and compliance.

What categories drive supermarket private label growth?

Private label growth in Romania is concentrated in:

Staple goods and protein remain dominant due to price sensitivity and volume stability.

Compliance and Certification Standards

Private label manufacturing in Romania requires:

-

IFS Food certification

-

BRCGS Food Safety

-

ISO 22000

-

HACCP systems

Large Romanian manufacturers maintain these certifications to qualify for supermarket contracts.

Conclusion

Romania’s private label manufacturing sector is concentrated among billion-RON protein processors and staple producers. Cris-Tim and Agricola now clearly lead the market by revenue scale, followed closely by Transavia. Their scale and integration make them structural partners within the wider Romanian supermarket ecosystem, where retailer own-brand penetration continues to expand.

Industrial integration, compliance readiness and national distribution capacity define supplier eligibility for modern retail private label contracts in 2026. As competition intensifies across the broader Romanian FMCG market, domestic manufacturers with certified production systems and stable supply chains remain best positioned to support supermarket private label growth.

Romanian-owned producers continue to play a central role in national supermarket supply chains, particularly across protein and staple categories.

Editor’s Note: This ranking is based on publicly available FY2024 financial disclosures and confirmed Romanian ownership as of early 2026. Only Romanian-owned food manufacturers with industrial-scale production relevant to supermarket private label supply were included.