Private label is no longer a side business in Portuguese supermarkets. It is now one of the strongest profit engines in food retail.

Across Portugal, own-brand products are growing faster than branded FMCG in many core categories. Retailers are using private label to control pricing, protect margins, and reduce dependence on multinational suppliers. This shift has placed Portugal above the European average in private label penetration for everyday grocery categories.

But power is not evenly spread.

Only a small group of supermarket operators truly control private label scale, manufacturing partnerships, and shelf dominance. These retailers decide which suppliers grow, which brands lose space, and which packaging formats become standard.

This ranking looks at the five retailers that shape Portugal’s private label market in 2026 and explains how their strategies are changing supplier economics, FMCG competition, and packaging demand.

Private Label Leaders (Portugal)

| Rank | Retailer | Private Label Share (Range) | Key Own Brands |

|---|---|---|---|

| 1 | Continente (Sonae MC) | High (over 30% of sales) | Continente, Continente Bio, Continente Seleção |

| 2 | Pingo Doce (Jerónimo Martins) | High (around 30%) | Pingo Doce Marca, Amanhecer Select |

| 3 | Lidl Portugal | Very High (over 70% of assortment) | Lidl own brand portfolio |

| 4 | Aldi Portugal | Very High (over 80% of assortment) | Aldi private labels |

| 5 | Intermarché Portugal | Medium to High | Poupança, regional ranges |

Note: Shares shown as ranges reflect public market positioning and category-level averages, not single audited figures.

Why private label matters more in Portugal

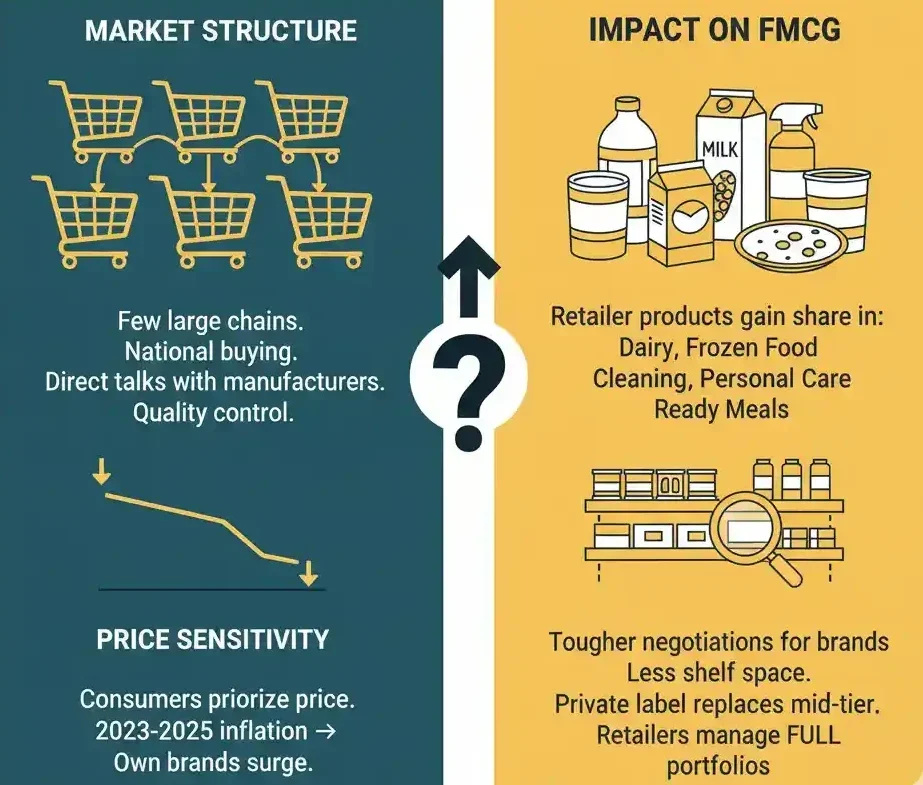

Portugal’s grocery market structure makes private label especially powerful.

The country is dominated by a few large chains with national buying platforms. This allows retailers to negotiate directly with manufacturers, control volume flows, and standardise product specifications.

At the same time, consumer behaviour in Portugal is highly price sensitive. Inflation pressure between 2023 and 2025 accelerated the shift toward own brands. Shoppers became more open to retailer products in dairy, frozen food, household cleaning, personal care, and ready meals.

This has changed FMCG in Portugal. Branded suppliers now face tougher listing negotiations, reduced shelf space, and more frequent private label replacement in mid-tier categories. Retailers are no longer just selling products. They are managing full product portfolios.

#1 Continente (Sonae MC)

Continente is the strongest private label operator in Portugal by scale and strategic depth.

Quality tiers

Continente runs a multi-tier private label system:

-

Entry price everyday ranges

-

Core mid-tier products

-

Premium lines such as Continente Seleção

-

Organic and wellness ranges like Continente Bio

This allows the retailer to capture different customer segments while keeping margin control inside its own brand ecosystem.

Price positioning

Continente uses private label to defend its price image against discounters while maintaining full-service supermarket positioning.

The retailer avoids extreme discount pricing. Instead, it focuses on value perception combined with quality signalling. Packaging design, ingredient claims, and regional sourcing labels are used to build trust without raising cost structure too high.

Supplier control

Sonae MC operates one of the most centralised buying systems in Portugal.

Suppliers working on Continente private label face:

-

High volume commitments

-

Standardised specifications

-

Long-term contracts with price pressure

-

Strict packaging and logistics requirements

This gives Continente strong leverage over manufacturers. It also shapes packaging in Portugal, as suppliers must adapt packaging formats, sustainability standards, and labelling rules set by the retailer.

#2 Pingo Doce (Jerónimo Martins)

Pingo Doce has built one of the most disciplined private label strategies in the Portuguese market.

Quality tiers

The retailer focuses heavily on its core brand range while expanding premium and fresh-oriented private label categories.

Key focus areas include:

-

Ready meals

-

Fresh prepared food

-

Bakery and chilled products

-

Mediterranean-style assortments

This fits Pingo Doce’s store format and urban footprint.

Price positioning

Pingo Doce uses aggressive promotional cycles supported by private label volume. Own-brand products allow the retailer to run weekly offers without relying fully on FMCG supplier funding.

This creates more internal pricing control and reduces dependence on brand promotions.

Supplier control

Jerónimo Martins has strong experience managing private label across multiple countries. This allows Pingo Doce to:

-

Use cross-border sourcing networks

-

Standardise product development

-

Negotiate scale-based manufacturing deals

For suppliers, this means strong volume opportunities but lower margin flexibility. It also influences packaging in Portugal, especially for chilled and ready meal categories where standard tray formats and label compliance are tightly controlled.

#3 Lidl Portugal

Lidl operates almost entirely on a private label model.

Quality tiers

Unlike full-line supermarkets, Lidl builds category portfolios around:

-

Entry price private labels

-

Core everyday ranges

-

Seasonal and premium temporary offers

This rotating structure keeps assortment tight and cost-efficient.

Price positioning

Lidl’s pricing strategy is based on cost leadership. Private label allows Lidl to remove brand marketing costs and negotiate direct production contracts.

This puts constant pressure on branded FMCG in Portugal, especially in categories like dairy, snacks, bakery, frozen food, and household products.

Supplier control

Lidl operates highly centralised European sourcing. Portuguese suppliers producing for Lidl must meet strict:

-

Cost targets

-

Packaging specifications

-

Sustainability compliance

-

Logistics standards

This has made Lidl one of the most influential buyers shaping supplier behaviour and packaging standards across Europe, including Portugal.

#4 Aldi Portugal

Aldi follows a similar private label-heavy strategy but with even tighter assortments.

Quality tiers

Aldi focuses on:

-

Core low-cost private labels

-

Limited premium seasonal lines

-

Simple packaging design

The strategy is built around operational efficiency rather than brand storytelling.

Price positioning

Aldi uses private label to deliver stable everyday pricing instead of heavy promotions. This appeals to value-driven shoppers and creates predictable demand patterns.

Supplier control

Supplier relationships are highly structured:

-

Fewer SKUs per category

-

High volume per product

-

Long production runs

This reduces complexity but limits supplier branding freedom. Packaging suppliers in Portugal working with Aldi often deal with simplified packaging formats designed for logistics efficiency.

#5 Intermarché Portugal

Intermarché operates under a cooperative model, which creates a different private label dynamic.

Quality tiers

Intermarché offers:

-

Core private label products

-

Regional and local supplier ranges

-

Price-focused entry tiers

This supports local sourcing but reduces standardisation compared to larger chains.

Price positioning

Intermarché balances national price competition with regional autonomy. Some stores adapt private label assortments based on local demand.

Supplier control

Supplier power is more distributed. This allows smaller Portuguese manufacturers to access shelf space but creates less unified volume leverage compared to Continente or Pingo Doce.

How private label Reshapes FMCG In Portugal

Private label growth is changing the structure of FMCG in Portugal.

Branded suppliers now face:

-

Reduced shelf space

-

Higher listing fees

-

More frequent delisting risk

-

Pressure to co-manufacture private label

Many FMCG companies now operate dual strategies. They sell branded products while also producing private label for retailers. This blurs the line between competition and partnership.

Retailers benefit because:

-

They control product pricing

-

They own consumer data

-

They manage promotional timing

-

They reduce dependency on multinational brand strategies

This shift is structural, not temporary.

How Private label Affects Packaging In Portugal

Private label also reshapes packaging demand.

Retailers increasingly:

-

Standardise packaging formats

-

Push lighter-weight materials

-

Demand recyclable or mono-material packaging

-

Control design guidelines

This forces packaging suppliers in Portugal to adapt production lines to retailer specifications rather than brand marketing requirements.

For packaging companies, private label contracts offer volume stability but lower margins. Design creativity is limited, while cost efficiency and sustainability compliance become critical.

This trend strengthens long-term partnerships between retailers and packaging suppliers while reducing flexibility for niche packaging formats.

Private Label Strategy Comparison

| Retailer | Value Tier Strength | Premium Tier Presence | Supplier Model |

|---|---|---|---|

| Continente | Strong | Strong | Centralised, long-term contracts |

| Pingo Doce | Strong | Medium to strong | Centralised sourcing network |

| Lidl | Very strong | Seasonal premium | Pan-European sourcing |

| Aldi | Very strong | Limited premium | Highly standardised sourcing |

| Intermarché | Medium | Regional focus | Cooperative supplier network |

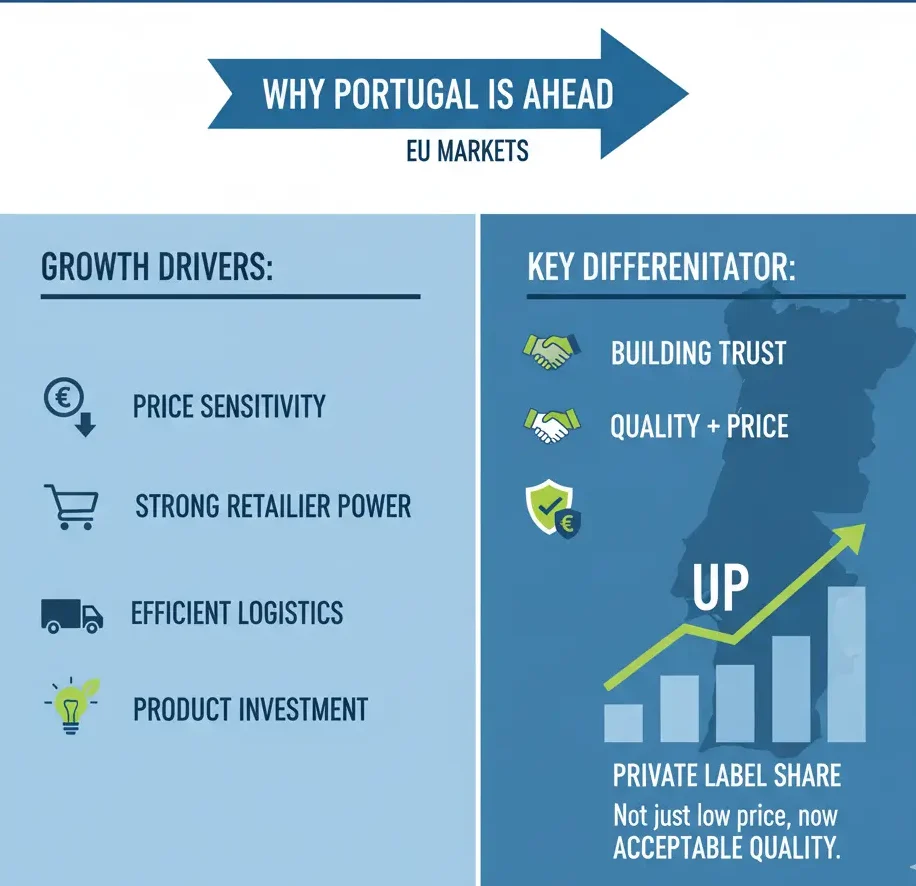

Why Portugal Is Ahead Of Many EU Markets

Portugal’s private label growth is driven by:

-

High price sensitivity

-

Strong supermarket concentration

-

Efficient national logistics networks

-

Retailer investment in product development

Unlike some Southern European markets where brands still dominate, Portuguese retailers have invested heavily in building trust in own brands.

Consumers now associate private label with acceptable quality, not just low price.

What suppliers must adapt to

Suppliers serving private label retailers in Portugal must adjust operations.

Key changes include:

-

Larger batch production

-

Flexible packaging formats

-

Lower per-unit margins

-

Higher compliance requirements

Manufacturers who fail to adapt risk losing access to national distribution.

What Happens Next

Private label will continue to expand across Portugal’s supermarkets.

Growth areas include:

-

Ready meals

-

Plant-based products

-

Health-focused categories

-

Sustainable packaging formats

Retailers will invest more in data-driven product development and category optimisation. Branded FMCG suppliers will face continued margin pressure.

For packaging companies, demand will grow for cost-efficient, standardised, recyclable packaging solutions designed for private label volume.

Private label is no longer optional. It is now the backbone of supermarket profitability.

Conclusion

The private label market in Portugal is controlled by a small group of powerful retailers.

Continente and Pingo Doce dominate full-line supermarket private label strategies. Lidl and Aldi lead the discount-driven model. Intermarché maintains a regional cooperative approach.

Together, these five players shape pricing, supplier economics, FMCG competition, and packaging standards across the country.

In 2026, own brands are no longer a secondary offer. They are the core business strategy of Portuguese food retail.

Editor’s Note: This analysis is based on publicly available retailer information, market structure data, and industry reporting on private label development in Portugal. Private label share figures are presented as ranges to reflect category-level variation and avoid overstating non-disclosed company data. The ranking focuses on strategic influence, assortment control, and supplier impact rather than short-term promotional performance.