Poland FMCG sector in 2026 is led by Maspex Group (PLN 16.0B), followed by dairy cooperatives Mlekovita and Mlekpol, and vertically integrated meat processor Animex Foods. The market structure combines strong domestic ownership with export-oriented dairy scale and increasing consolidation in protein and beverage manufacturing.

Quick Facts

-

Largest FMCG company in Poland: Maspex Group (PLN 16.0B, FY2024)

-

Dairy cooperatives account for two of the top four positions

-

Meat processing is increasingly consolidated under multinational ownership

-

Beverage and convenience categories show continued regional expansion

-

Packaging integration is structurally important under EU circular economy regulation

-

Export exposure remains a defining growth driver across major producers

Top 10 FMCG Companies in Poland (Ranked by FY2024 Revenue)

| Rank | Company | FY2024 Revenue (PLN) | Key Update / Status |

|---|---|---|---|

| 1 | Maspex Group | PLN 16.0B | Record revenue; continued regional expansion |

| 2 | Mlekovita | PLN 11.0B+ | Dairy cooperative exporting to 160+ markets |

| 3 | Animex Foods | ~PLN 11.5B* | Vertically integrated; owned by WH Group |

| 4 | Mlekpol | PLN 8.0B+ | Major UHT milk and cheese exporter |

| 5 | Grupa Kęty | PLN 5.1B (Group) / ~PLN 1.1B (Packaging) | Packaging division supports FMCG circular compliance |

| 6 | Żywiec Group | PLN 4.0B+ | Polish beer leader; part of Heineken group |

| 7 | Indykpol (LDC Group) | PLN 3.0B+ | Fully consolidated by French LDC Group (Aug 2024) |

| 8 | Wedel | PLN 2.2B | Ongoing factory expansion investment |

| 9 | Colian Holding | PLN 1.7–1.8B | Acquired Gubor Schokoladen (April 2025) |

| 10 | Bakalland (FoodWell Group) | PLN 2.0B+ | Health snack focus; operating under FoodWell structure |

*Animex turnover converted from USD to PLN using average 2024 exchange rate. See Editor’s Note.

1. Maspex Group

Founded: 1990

Headquarters: Wadowice

Maspex reported PLN 16.0 billion in revenue for FY2024, confirming its position as Poland’s largest FMCG manufacturer.

Core categories:

-

Juices and soft drinks

-

Energy beverages

-

Pasta and ready meals

-

Sauces and processed foods

Maspex operates across Central and Eastern Europe and continues expanding through acquisitions. Its scale reinforces strong supermarket leverage and distribution efficiency across beverage and convenience categories.

2. Mlekovita

Founded: 1928

Headquarters: Wysokie Mazowieckie

Mlekovita remains Poland’s largest dairy cooperative, with revenue exceeding PLN 11 billion in 2024.

Core categories:

-

UHT milk

-

Cheese

-

Butter

-

Milk powders

The cooperative model secures raw milk supply through farmer integration. Export operations extend across Europe, Asia, and Africa, strengthening Poland’s dairy trade position.

3. Animex Foods

Ownership: WH Group (Smithfield)

Animex generated approximately USD 3.0 billion in 2024 turnover, equivalent to roughly PLN 11.5 billion.

Core categories:

-

Pork

-

Processed meats

-

Poultry

Animex operates vertically integrated meat production and distribution. Protein remains one of Poland’s highest-value supermarket categories, and Animex maintains structural influence in chilled and processed segments.

4. Mlekpol

Founded: 1979

Headquarters: Grajewo

Mlekpol ranks as Poland’s second-largest dairy cooperative.

Core categories:

-

Milk

-

Cheese

-

Yogurts

-

Milk powders

The company holds strong export positioning and maintains extensive domestic supermarket penetration.

5. Grupa Kęty

Founded: 1953

Headquarters: Kęty

Grupa Kęty reported total group revenue of approximately PLN 5.1 billion in FY2024. While the company operates primarily as an aluminium processing group, its Flexible Packaging Segment — generating roughly PLN 1.1 billion — is directly relevant to Poland’s FMCG manufacturing and retail supply chains.

Core areas relevant to FMCG:

-

Flexible food packaging

-

Laminates and aluminium-based materials

-

Barrier packaging solutions

-

Industrial packaging components

The packaging division supplies materials used in food, dairy, confectionery, and ready-meal categories. Material performance, lightweighting, and recyclability are increasingly critical under evolving EU circular economy regulation.

As sustainability reporting and packaging compliance tighten across Europe, domestic packaging capacity becomes strategically important. Grupa Kęty’s integration within the Polish industrial base supports supply stability and reduces exposure to cross-border material volatility.

Packaging is no longer peripheral to FMCG manufacturing economics. Cost structure, regulatory compliance, and recycling targets are now embedded in production planning, reinforcing the structural relevance of packaging suppliers within Poland’s grocery ecosystem.

6. Żywiec Group

Żywiec remains one of Poland’s leading beer producers.

Core categories:

-

Lager

-

Premium beer

-

Specialty brews

Beer maintains strong retail presence, particularly in premium segments.

7. Indykpol

8. Wedel

Founded: 1851

Headquarters: Warsaw

Wedel reported approximately PLN 2.2 billion in FY2024 revenue, maintaining its position as one of Poland’s leading confectionery manufacturers. The company operates modern production facilities in Poland and continues investing in capacity upgrades to support both domestic demand and export growth.

Core categories:

-

Chocolate bars and tablets

-

Boxed confectionery

-

Seasonal chocolate products

-

Premium cocoa-based sweets

Confectionery remains a relatively value-stable category within Polish retail, particularly in premium and seasonal segments. Wedel’s brand recognition supports consistent supermarket shelf presence, while factory expansion investments aim to improve efficiency, automation, and export capability.

As private-label competition increases in mainstream sweets, branded chocolate manufacturers such as Wedel rely on premium positioning, product innovation, and export diversification to sustain margin performance within Poland’s FMCG landscape.

9. Colian Holding

10. Bakalland (FoodWell Group)

Founded: 1991

Headquarters: Warsaw

Operating under the FoodWell Group structure, Bakalland remains one of Poland’s leading producers of nuts, dried fruits, and functional snack products. The company has repositioned itself within the broader health and wellness segment, aligning with shifting consumer demand patterns.

Core categories:

-

Packaged nuts

-

Dried fruits

-

Snack bars and protein products

-

Private-label healthy snacks

Health-oriented packaged snacking continues gaining retail shelf share across Polish supermarkets. Demand for portion-controlled, protein-enriched, and plant-based snack formats has supported category premiumisation.

Bakalland’s integration within FoodWell reflects a strategic focus on brand consolidation and portfolio simplification. As supermarkets expand better-for-you assortments and private-label health ranges, suppliers positioned in functional snacking are increasingly relevant within Poland’s evolving FMCG landscape.

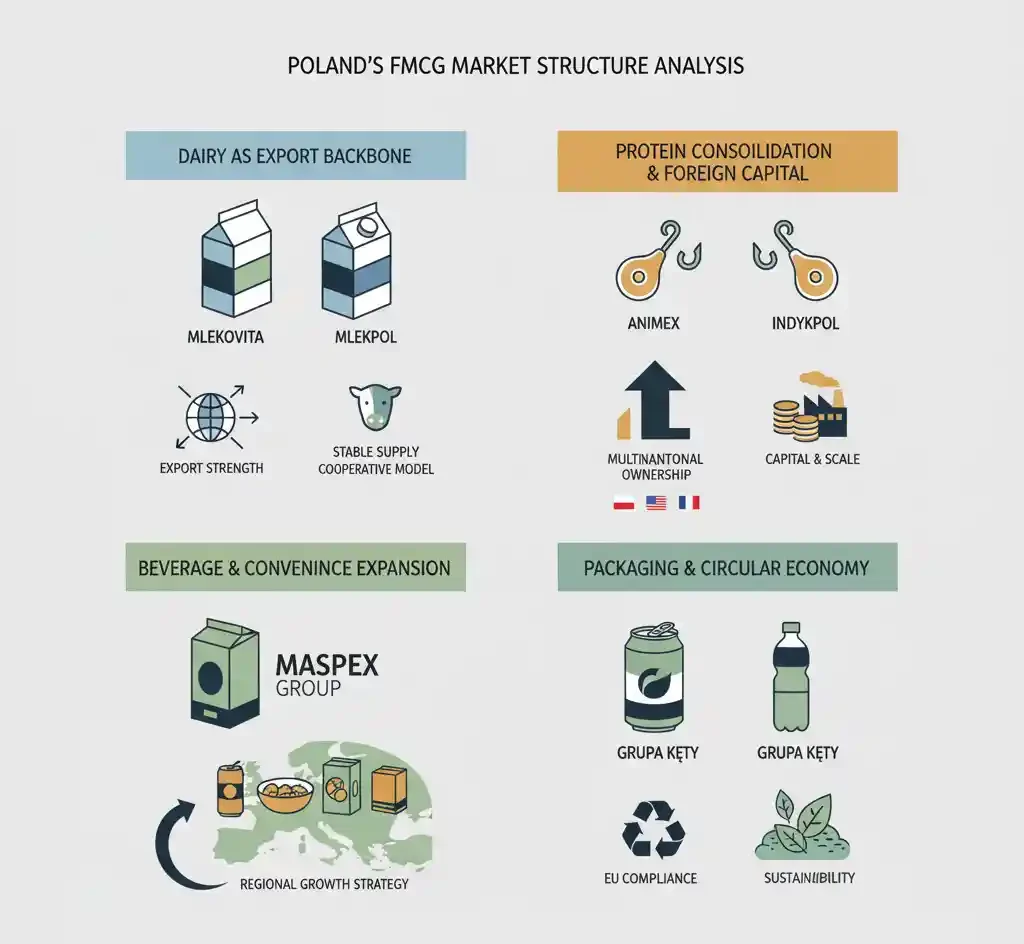

Market Structure Analysis

Dairy as Export Backbone

Two cooperatives occupy top-tier positions, highlighting Poland’s dairy export strength. Cooperative ownership stabilizes raw material supply and reduces exposure to commodity volatility.

Protein Consolidation and Foreign Capital

Animex and Indykpol reflect increasing multinational ownership within Polish protein production. Consolidation strengthens capital access and operational scale while maintaining domestic manufacturing bases.

Beverage and Convenience Expansion

Maspex’s leadership demonstrates how beverage and ready-meal categories are driving revenue scale. Regional expansion remains central to growth strategy.

Packaging and Circular Economy Compliance

Grupa Kęty’s packaging division underlines the increasing importance of material sourcing, aluminium recycling, and EU compliance requirements across FMCG supply chains.

Industry Outlook 2025–2027

Poland’s FMCG manufacturing landscape is shaped by:

-

Automation and cost-efficiency investments

-

Export market diversification

-

Private-label growth

-

EU circular economy compliance

Production integration, supply chain resilience, and scale efficiency will remain defining competitive factors.

Conclusion

The top FMCG companies in Poland combine cooperative dairy strength, vertically integrated protein processing, beverage consolidation, and packaging alignment. Revenue concentration among leading players reflects structural maturity within the Polish grocery manufacturing ecosystem and its close integration with the broader Poland supermarket network.

As consolidation continues and regulatory pressures increase, operational scale and export positioning will define long-term leadership. Developments in Poland packaging compliance and private-label expansion across domestic retail chains are expected to further shape competitive positioning in the coming years.

Editor’s Note: All revenue figures are based on publicly available company financial disclosures. Animex turnover was converted from USD to PLN using average 2024 exchange rates for consistency. Packaging division revenue for Grupa Kęty reflects segment reporting within group results. No assumptions or projected figures have been included.