Romania FMCG sector in 2026 is driven by operational strength, not marketing visibility. The market is shaped by packaging compliance rules, the national deposit-return system (SGR), private label growth, and ongoing supermarket consolidation. These factors now define which companies have real retail influence.

While multinational groups operate in the country, a core group of Romanian-founded and Romanian majority-controlled manufacturers continues to anchor supermarket supply across beverages, poultry and processed meat, frozen foods, canned and ambient products, flour, pasta, and other staple categories.

In Romania, FMCG (Fast-Moving Consumer Goods) companies are producers of high-turnover food and beverage items sold through supermarkets, hypermarkets, discounters, and convenience chains.

This ranking includes only companies that were founded in Romania and remain Romanian majority-controlled in 2026. It excludes foreign-owned subsidiaries, supermarket chains, cash and carry operators, and pure commodity traders without consumer-facing FMCG brands.

The ranking is based strictly on FY2024 turnover, using revenue figures reported in Romanian lei (RON). Where companies operate through multiple legal entities, group-level figures are used to reflect real market scale. Employee numbers reflect the latest publicly disclosed headcount, and ownership status has been verified for 2026.

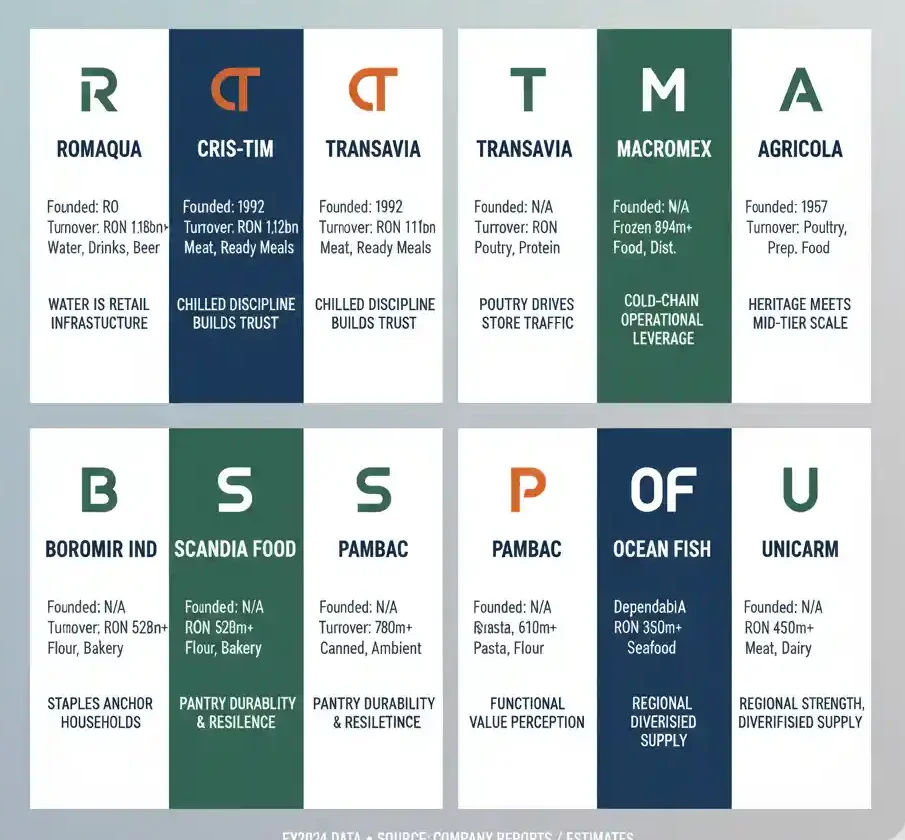

Revenue Ranking – Romanian-Owned FMCG Leaders (FY2024)

| Rank | Company | FY2024 Turnover (RON) | Total Employees | Core Strength | Retail Influence Indicator |

|---|---|---|---|---|---|

| 1 | Romaqua Group | 1,181,776,334 | ~2,000+ | Bottled water, beverages | National beverage infrastructure + SGR exposure |

| 2 | Cris-Tim Family Holding | ~1,120,000,000 | ~2,500+ | Processed meat, ready meals | Chilled category block power |

| 3 | Transavia | ~1,115,000,000 | ~2,200+ | Poultry | Protein anchor for modern retail |

| 4 | Macromex | 894,023,029 | ~1,000+ | Frozen foods | Freezer distribution control |

| 5 | Agricola International | 806,601,725 | ~2,000+ | Poultry, prepared foods | Integrated protein operations |

| 6 | Boromir Ind | 528,238,299 | ~1,500+ | Milling, bakery | Staple basket stability |

| 7 | Scandia Food (Group) | 780,000,000+ | ~1,200 | Canned / ambient / frozen | Pantry resilience |

| 8 | Pambac (Group) | 610,000,000+ | ~900+ | Pasta, flour | Value-led staple reach |

| 9 | Unicarm (Manufacturing Group) | 450,000,000+ | ~1,100 | Meat & dairy | Regional-to-national expansion |

| 10 | Ocean Fish (Group) | 350,000,000+ | ~600+ | Seafood | Category captain role |

Why Employees Matter for Scale

The SGR Impact: A Structural Shift

Romania’s Sistemul Garanție-Returnare (SGR) became fully operational across beverage categories in 2024–2025, creating a structural shift in the FMCG market. Beverage producers were required to redesign packaging, apply deposit-marked labeling, coordinate reverse logistics systems, and manage cash flow linked to deposit circulation.

Compliance with SGR is no longer optional; it has become a measurable factor of operational strength. Retailers increasingly prefer suppliers that can execute the deposit-return process smoothly, reducing in-store complexity and administrative pressure. In 2026, packaging readiness and SGR compliance directly influence commercial negotiations and supplier selection in modern retail.

Company Profiles (Expanded – 2026 Analysis)

1. Romaqua Group

Founded: Romanian-founded beverage group

FY2024 Turnover: RON 1.18bn+

Employees: ~2,000+

Core categories: Mineral water, carbonated drinks, beer

Romaqua sits at the top of the domestic FMCG hierarchy primarily because water is not just a product category — it is retail infrastructure. Bottled water is one of Romania’s highest-volume, highest-frequency SKUs across modern retail formats.

The group’s scale is built around:

-

Multiple bottling facilities across Romania

-

National distribution reach

-

Strong presence in both hypermarkets and discount formats

Water is pallet-heavy and logistically demanding. That creates entry barriers. Retailers depend on suppliers that can maintain uninterrupted volume, particularly during summer peaks and promotional weeks.

Retail Influence Factors

-

Water shapes price perception. Retailers use it as a value signal.

-

Promotional mechanics in beverages are constant and margin-sensitive.

-

SGR (Deposit-Return System) exposure has increased operational complexity.

Romaqua’s packaging readiness and compliance capability under SGR made it operationally indispensable to retailers in 2025–2026. That alone reinforces its negotiating strength.

In practical terms: if water supply fails, stores feel it immediately. That is structural influence.

2. Cris-Tim Family Holding

Founded: 1992

FY2024 Turnover: ~RON 1.12bn

Employees: ~2,500+

Core categories: Processed meat, ready meals, chilled proteins

Cris-Tim operates in one of the most execution-sensitive areas of retail: chilled processed foods. These categories carry:

-

High shrink risk

-

Strict cold-chain requirements

-

Rapid promotional cycles

Scale in chilled FMCG is less about marketing and more about discipline. Cris-Tim’s footprint allows it to hold large blocks of planogram space in major chains.

Retail Influence Factors

-

High SKU density in chilled cabinets

-

Ability to support national promotions

-

Manufacturing scale to absorb margin pressure

Private label competition is strong in processed meat. However, large domestic producers often operate across both branded and contract manufacturing segments, which increases strategic value to retailers.

Chilled reliability builds trust. In Romanian supermarkets, that trust translates directly into shelf permanence.

3. Transavia

Founded: Early 1990s

FY2024 Turnover: ~RON 1.11bn

Employees: ~2,200+

Core categories: Poultry, fresh protein

Protein categories define weekly basket economics. Poultry, in particular, influences:

-

Consumer price perception

-

Traffic patterns

-

Cross-category spending

Transavia’s vertical integration strengthens its ability to stabilise supply even during feed or energy volatility.

Retail Influence Factors

-

Volume reliability

-

Capacity to support weekly discount mechanics

-

Integrated farm-to-processing operations

In Romania, poultry remains the mainstream protein. Retailers protect stable poultry partnerships because disruptions directly impact store traffic and customer satisfaction.

Transavia’s scale makes it a core supplier rather than a replaceable one.

4. Macromex

FY2024 Turnover: 894m+ RON

Employees: ~1,000+

Core categories: Frozen foods, distribution

Macromex represents a different kind of FMCG influence — control of cold-chain distribution in frozen categories.

Frozen categories require:

-

Stable freezer infrastructure

-

Precise logistics

-

Seasonal volume planning

Retailers cannot rotate frozen suppliers easily because freezer capacity is limited and operational complexity is high.

Retail Influence Factors

-

Control of freezer assortment flow

-

Execution capability during seasonal peaks

-

Ability to manage branded and distributed portfolios

In practical retail terms, frozen influence is about what actually reaches the freezer cabinet consistently. That is operational leverage.

5. Agricola International

Founded: 1957

FY2024 Turnover: 806m+ RON

Employees: ~2,000+

Core categories: Poultry, prepared foods

Agricola combines heritage with scale. It operates in both fresh protein and value-added prepared food segments, bridging price-sensitive and convenience-driven consumers.

Retailers value suppliers who can:

-

Support mid-tier price architecture

-

Offer cross-category SKUs

-

Maintain production stability during volatility

Agricola’s structure allows it to serve both large hypermarkets and smaller regional chains without overconcentration in one format.

Its retail role is structural, not seasonal.

6. Boromir Ind

FY2024 Turnover: 528m+ RON

Employees: ~1,500+

Core categories: Milling, flour, bakery

Staples rarely make headlines but always move volume.

Boromir’s milling operations support:

-

Branded flour

-

Bakery-linked packaged goods

-

Private label supply

In economic uncertainty, staple categories gain relative strength. Flour and basic bakery products anchor household cooking patterns.

Retail Influence Factors

-

Wide distribution coverage

-

Integration with private label programs

-

Stable replenishment cycles

Staple suppliers become part of supermarket baseline assortment — rarely rotated out unless performance collapses.

7. Scandia Food

FY2024 Turnover: 780m+ RON (Consolidated Group)

Employees: ~1,200

Core categories: Canned and ambient foods

Ambient categories support stock-up behaviour. Canned foods provide long shelf life and budget stability for households.

Scandia’s position in pantry categories offers:

- Resilience during price-sensitive cycles

- Lower shrink risk for retailers

- Broad SKU rotation across store formats

Ambient shelf space is competitive but stable. Once brands establish trust, retailers tend to keep them.

This creates medium-term retail durability.

8. Pambac

FY2024 Turnover: 610m+ RON (Consolidated Group)

Employees: ~900+

Core categories: Pasta, flour

Pasta and flour are price-sensitive categories that influence value perception.

Retailers use these categories to signal affordability. Suppliers capable of:

- Supporting price ladders

- Maintaining consistent quality

- Delivering stable supply

gain shelf consistency.

Pambac’s role is functional rather than flashy — but in supermarket strategy, functional matters.

9. Ocean Fish

FY2024 Turnover: 350m+ RON (Consolidated Group)

Employees: ~600+

Core categories: Seafood

Seafood is operationally demanding:

- Cold-chain integrity

- Short shelf life

- Import exposure

Retailers prefer partners who manage sourcing complexity reliably.

Ocean Fish’s retail influence is built on:

- Category reliability

- Breadth of assortment

- Execution stability

In seafood, a few dependable suppliers often control most of the visible range.

10. Unicarm

FY2024 Turnover: 450m+ RON (Manufacturing Group)

Employees: ~1,100+

Core categories: Meat and dairy

Unicarm combines regional strength with expanding distribution reach.

Its relevance lies in:

- Mid-market pricing

- Regional manufacturing base

- Ability to serve multiple store formats

Retailers often balance national giants with strong regional players to diversify supply risk. Unicarm fits that structural role.

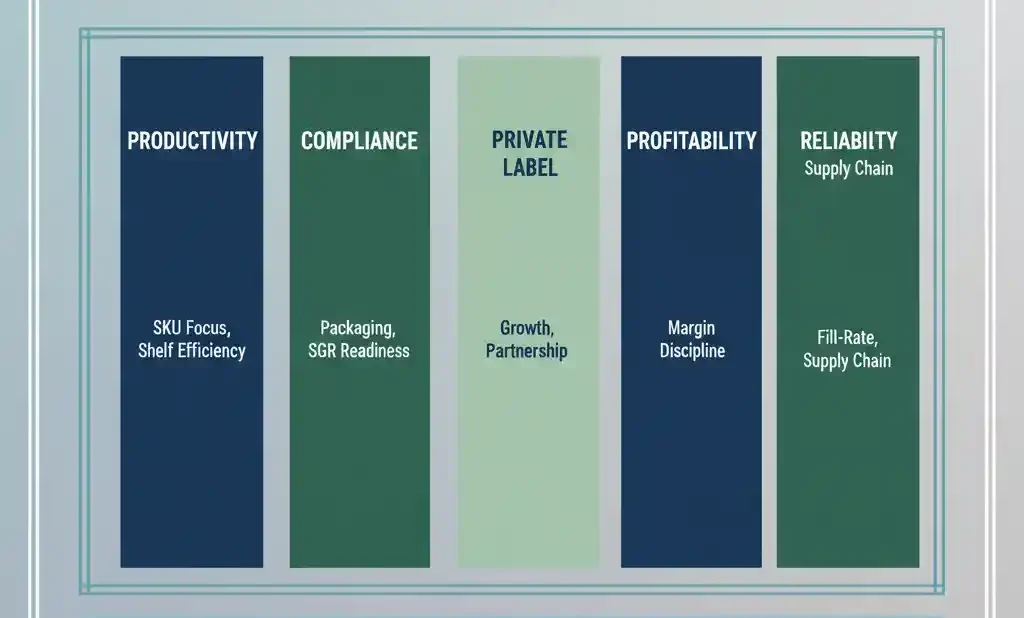

Market Structure Insights (2026)

Supermarket negotiations in 2026 focus on:

-

SKU productivity

-

Packaging compliance

-

Private label expansion

-

Margin discipline

-

Fill-rate reliability

Romanian-owned manufacturers with integrated production and stable distribution remain embedded in retail systems.

Conclusion

The top 10 FMCG companies in Romania by revenue, scale and retail influence show that domestic industrial capacity remains central to Romanian supermarket supply chains. These manufacturers are not just brand owners; they are structural suppliers that keep shelves filled across national hypermarkets, discounters and regional chains.

Romaqua leads by turnover and beverage infrastructure exposure, particularly within categories shaped by the national deposit-return system. Protein producers follow closely, reinforcing the core of the Romanian supermarket fresh and chilled offer. Staples, frozen and ambient players provide the volume stability that underpins everyday basket demand.

In 2026, retail influence in Romania is defined less by advertising strength and more by operational reliability, manufacturing scale and Romanian packaging compliance capability. Supermarkets increasingly prioritise suppliers that can deliver consistent fill rates, manage SGR requirements and maintain production stability in a margin-sensitive environment.

Editor’s Note: All turnover and employee figures are based on publicly available FY2024 financial disclosures and verified 2026 ownership status. Revenue is presented in RON as officially reported. No projections or currency conversions were used.