Sweden’s retail sector enters 2026 with one of Europe’s most digitised store environments.

Electronic shelf labels are embedded across grocery.

Self-checkout systems are standard in urban supermarkets.

Unified commerce platforms connect store and online inventory in real time.

Retail technology in Sweden is no longer innovation-led experimentation. It is structural infrastructure tied directly to margin control, automation, and regulatory compliance.

The ranking below reflects the latest publicly available FY2024 and LTM 2025 disclosures, prioritising confirmed revenue scale.

Revenue & Core Technology (FY2024–LTM 2025)

| Rank | Company | Revenue (Latest FY / LTM 2025) | Status | Core Retail Technology |

|---|---|---|---|---|

| 1 | ITAB Group | ~SEK 12–13bn (FY2025 trajectory) | Nasdaq Stockholm | Store solutions, automation, checkout |

| 2 | Pricer | ~SEK 2.2–2.5bn (LTM Q3 2025) | Nasdaq Stockholm | Electronic shelf labels |

| 3 | Extenda Retail | ~SEK 1.5bn+ (FY2024 scale est.) | Private (STG) | POS, unified commerce |

| 4 | Avensia | ~SEK 430–450m (FY2024–LTM 2025) | Nasdaq First North | Commerce integrations |

| 5 | Sitoo | ~SEK 250–300m ARR (2026 est.) | Private | Cloud-native POS |

| 6 | Bambuser | ~SEK 85–100m (FY2024–LTM 2025) | Nasdaq First North | Live shopping SaaS |

| 7 | Voyado | Revenue undisclosed | Private | CRM & loyalty automation |

| 8 | Centiro | Revenue undisclosed | Private | OMS & logistics tech |

| 9 | StrongPoint (Sweden ops) | Nordic group reporting | Oslo-listed | Store automation |

| 10 | Zettle (PayPal) | Within PayPal reporting | Subsidiary | POS & payments |

Company Profiles

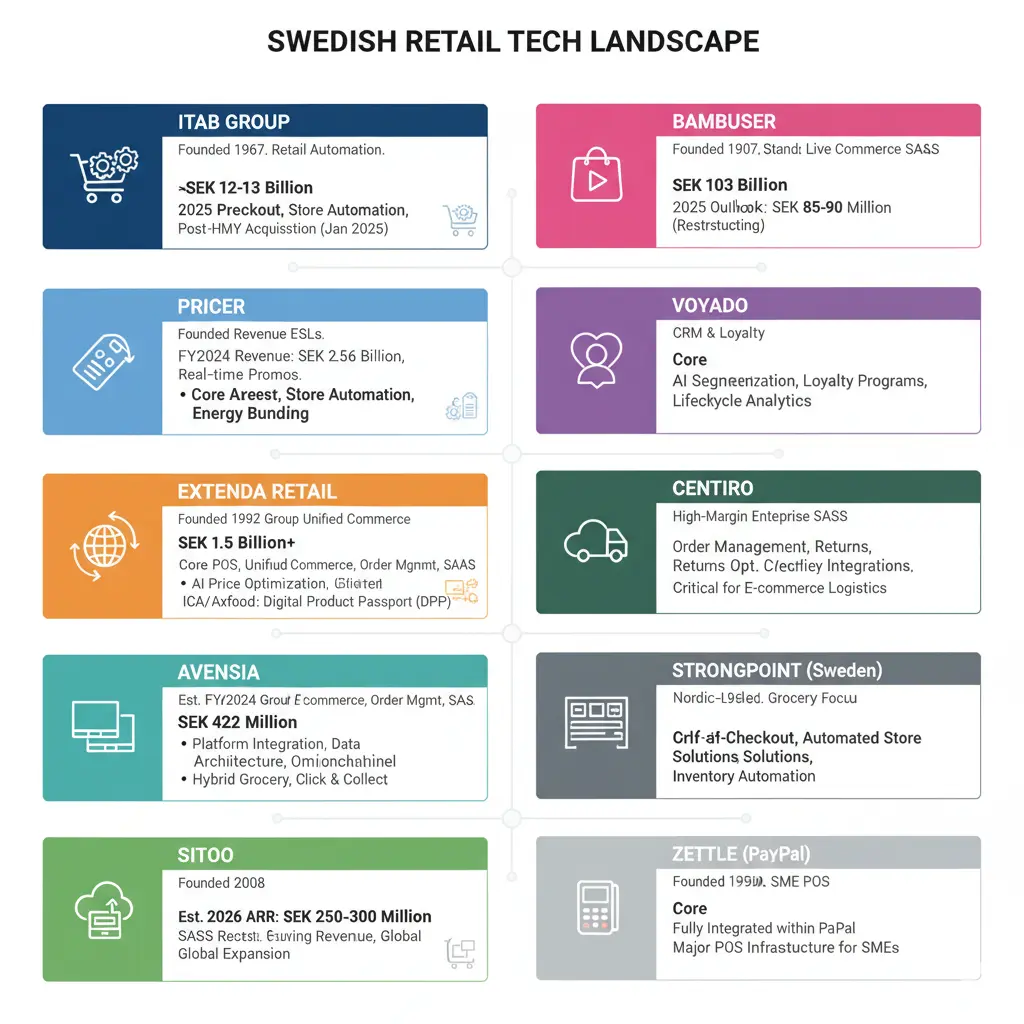

1. ITAB Group

Founded in 1967 in Jönköping.

ITAB evolved from store fixture manufacturing into a full retail automation provider.

The turning point was the acquisition of HMY, completed January 2025.

For Jan–Sep 2025, pro-forma net sales reached SEK 9.85 billion.

Full-year 2025 trajectory places revenue comfortably in the SEK 12–13 billion range.

Core areas:

Self-checkout systems

Cash management

Store automation

Energy-efficient store concepts

Market structure:

ITAB now exceeds the combined revenue of most other Swedish retail tech firms.

Strategic focus:

Integration of HMY.

Global expansion.

Automation bundling.

2. Pricer

Founded in 1991.

Pricer is Sweden’s largest pure-play electronic shelf label supplier.

FY2024 revenue: SEK 2.56 billion.

LTM Q3 2025: approximately SEK 2.2 billion.

While revenue softened from its 2024 peak, order intake and gross margins improved into 2026.

Core technology:

ESL infrastructure

Cloud-connected digital pricing

Real-time promotional updates

Structural relevance:

AI-driven price optimisation is increasingly integrated into Pricer’s cloud ecosystem.

Retail chains such as ICA and Axfood are expanding ESL-linked automation as CapEx priorities shift toward pricing agility.

3. Extenda Retail

Founded in 1982.

Extenda developed from Swedish POS systems into a global unified commerce provider.

Estimated group revenue scale: SEK 1.5bn+ (industry consensus FY2024).

Core:

POS platforms

Unified commerce systems

Order management

SaaS architecture

Market reach:

Operations across 35+ countries.

Compliance relevance:

Supports Digital Product Passport (DPP) data integration at store level.

4. Avensia

Founded in 2008 in Lund.

FY2024 revenue: SEK 422 million.

LTM 2025: approximately SEK 432 million.

Core services:

Commerce platform integration

Retail data architecture

Omnichannel transformation

Operational impact:

Supports hybrid grocery models and click-and-collect systems.

5. Sitoo

Founded in 2008, Stockholm.

Private company focused on cloud-native POS.

Estimated ARR scale: SEK 250–300 million entering 2026.

Market view:

Often cited as the fastest-growing cloud POS provider in the Nordics.

Strategic direction:

SaaS-based recurring revenue and international expansion.

6. Bambuser

Founded in 2007.

Pivoted from live streaming into retail live commerce SaaS.

FY2024 revenue: SEK 103 million.

2025 outlook: SEK 85–90 million amid restructuring.

Strategic shift:

Transition toward high-margin enterprise SaaS contracts rather than broad consumer volume growth.

7. Voyado

Founded in 2005.

Private CRM and loyalty technology company.

Revenue not publicly disclosed.

Market perception:

Considered the Nordic market standard for fashion and specialty retail CRM.

Core:

AI-driven segmentation

Loyalty programs

Customer lifecycle analytics

8. Centiro

Founded in 1998, Borås.

Focus:

Order management

Returns optimisation

Carrier integrations

Supports more than 300 global brands.

Role in retail:

Critical in logistics-heavy e-commerce operations.

9. StrongPoint (Sweden Operations)

Nordic-listed provider with strong Swedish grocery deployments.

Core:

Self-checkout

Automated store solutions

Often aligned with inventory automation initiatives.

10. Zettle (PayPal)

Founded in Stockholm in 2010.

Now fully integrated within PayPal.

Standalone Sweden revenue not separable.

Market impact:

Major POS infrastructure provider for SMEs.

Market Structure Impact

Revenue concentration in 2026 is decisive.

ITAB’s scale following the HMY integration creates a hardware-dominant structure.

Software-driven firms operate with lower absolute revenue but higher margin SaaS models.

The market now reflects:

Hardware scale leadership

Software recurring revenue specialists

Category Dominance Trends

Electronic Shelf Labels

Pricer remains Sweden’s flagship ESL provider.

Unified Commerce

Extenda and Sitoo drive SaaS transformation.

Store Automation

ITAB and StrongPoint support inventory and checkout automation.

CRM & Loyalty

Voyado defines Nordic data-driven retail engagement.

Live Commerce

Bambuser reflects the post-pandemic normalisation of live retail.

AI Efficiency & CapEx Drivers (2026 Shift)

Automation in 2026 is increasingly AI-driven.

Retailers prioritise:

AI-based price optimisation integrated with ESL platforms

Automated replenishment systems

Data-driven checkout staffing models

Investment cycles in Swedish grocery now focus on measurable efficiency returns rather than expansion of physical store space.

Sustainability & Digital Product Passport Impact

EU Digital Product Passport (DPP) regulations are reshaping retail tech procurement.

Swedish retailers require:

Traceability data integration

Digital compliance labelling

Product-level transparency

Technology providers such as Pricer and Extenda are winning contracts partly due to DPP compatibility.

Sustainability compliance is no longer CSR positioning. It is regulatory necessity.

Industry Outlook 2026–2028

Three structural forces define the next phase:

Hardware-software integration

AI-driven automation

Regulatory compliance technology

Swedish retail technology companies increasingly export solutions across Europe and North America.

Domestic grocery groups remain anchor clients, but growth trajectories are international.

Conclusion

Editor’s Note: Financial data is based on publicly available FY2024 and LTM/Q3 2025 company disclosures. Private company figures are industry estimates where clearly indicated. All revenue values are presented in SEK with no currency conversion applied.