Finland has one of the most concentrated grocery retail markets in Europe.

A small number of supermarket groups control almost all national grocery sales.

This structure is not new, but it has become more pronounced over the past decade.

Scale, logistics efficiency, private label development, and buying power now define competitive advantage.

This article ranks the top five supermarket groups in Finland by grocery market share, using the latest publicly available data.

The ranking is strictly based on market share, not store count or brand visibility.

Together, these five groups account for more than 95% of Finnish grocery retail sales.

Beyond them, remaining operators are marginal at national level.

Finland grocery retail at a glance

Finland’s grocery market is shaped by geography, population density, and long-established retail models.

Key characteristics:

- High national concentration

- Strong cooperative and retailer-led structures

- Deep private label penetration

- Centralised procurement and logistics

Two domestic groups dominate.

One international discount chain has secured a stable third position.

The remaining players operate at much smaller scale.

This concentration has direct implications for:

- Supplier negotiations

- Packaging volumes

- Logistics network design

- Category access and shelf space

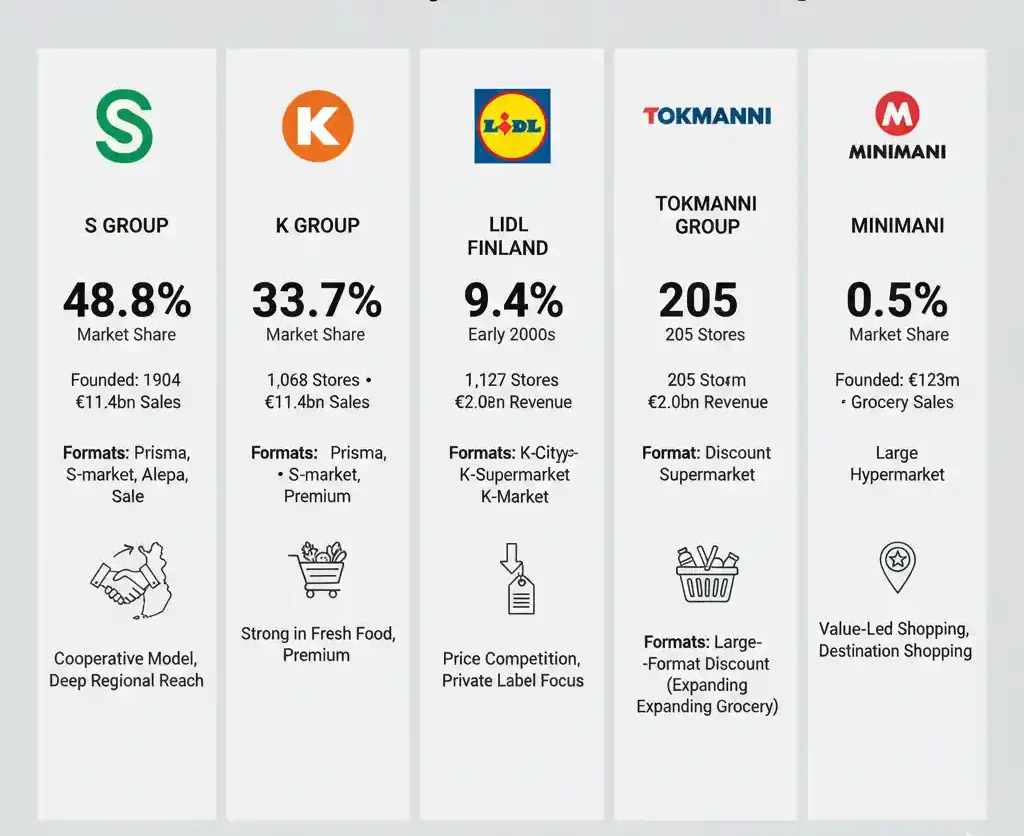

5 supermarket groups in Finland (by market share)

| Rank | Supermarket group | Market share | Grocery revenue* | Stores | Employees |

|---|---|---|---|---|---|

| 1 | S Group | 48.8% | €11.4bn | 1,068 | 40,000+ |

| 2 | K Group | 33.7% | €7.9bn | 1,127 | 39,000 |

| 3 | Lidl Finland | 9.4% | €2.0bn | 205 | 5,700+ |

| 4 | Tokmanni Group | 3.3% | €0.76bn | 205 | 6,600+ |

| 5 | Minimani | 0.5% | €0.12bn | 7 | ~350 |

Grocery revenue figures reflect the latest publicly available fiscal-year grocery sales data.

1. S Group

Founded in 1904, S Group is a consumer-owned cooperative network.

It is the clear market leader in Finnish grocery retail.

With 48.8% market share, S Group alone accounts for nearly half of all grocery sales in the country.

Core grocery formats

- Prisma (hypermarket)

- S-market (supermarket)

- Alepa and Sale (convenience)

Scale and operations

- 1,068 grocery stores nationwide

- €11.4bn in grocery sales

- 40,000+ employees

S Group’s cooperative structure gives it deep regional coverage.

Local cooperatives operate stores but benefit from central procurement, logistics, and private label development.

Market position

S Group sets the reference point for pricing, assortment breadth, and private label standards in Finland.

Its buying power is unmatched.

Suppliers often treat S Group negotiations as the baseline for the entire Finnish market.

Operational relevance

- High-volume packaging demand

- Centralised distribution centres

- Strong private label programmes across food and non-food

S Group’s decisions often ripple through supplier pricing models and logistics planning.

2. K Group (Kesko grocery)

K Group’s grocery business is operated through Kesko and independent K-retailers.

The group was established in 1940.

With 33.7% market share, K Group is the second pillar of Finnish grocery retail.

Core grocery formats

- K-Citymarket (hypermarket)

- K-Supermarket

- K-Market (convenience and neighbourhood)

Scale and operations

- 1,127 stores, the largest network by count

- €7.9bn in grocery sales

- ~39,000 employees

The K-retailer model allows store-level flexibility while maintaining centralised purchasing power.

Market position

K Group competes directly with S Group across all major categories.

It is particularly strong in fresh food, premium ranges, and urban locations.

Retailer entrepreneurship leads to variation between stores.

This can benefit suppliers with differentiated or local offerings.

Operational relevance

- Complex assortment structures

- High SKU diversity

- Strong demand for packaging customisation

For many suppliers, K Group requires tailored commercial strategies compared with S Group.

3. Lidl Finland

Lidl entered Finland in the early 2000s as part of its wider European expansion.

It is a wholly owned subsidiary of the Schwarz Group.

Today, Lidl holds 9.4% market share, making it the third-largest grocery retailer in Finland.

Core grocery format

- Discount supermarket (single-format model)

Scale and operations

- 205 stores

- ~€2.0bn in Finnish revenue

- 5,700+ employees

Lidl operates a lean, standardised store model.

Assortments are limited compared with Finnish competitors.

Market position

Lidl has reshaped price competition in Finland.

Its presence forced domestic retailers to strengthen entry-price and private label tiers.

Growth has slowed in recent years, but Lidl remains structurally important.

Operational relevance

- Centralised European sourcing

- High private label share

- Large-volume, standardised packaging runs

For international suppliers, Lidl Finland often fits into broader Nordic or European supply frameworks.

4. Tokmanni Group

Tokmanni was founded in 1989 and built its reputation in non-food discount retail.

Its grocery offer has expanded steadily over time.

The group now holds 3.3% market share in Finnish grocery retail.

Core formats

- Large-format discount stores

- Expanding everyday grocery sections

Scale and operations

- 205 stores

- €764m in grocery sales

- 6,600+ employees

Tokmanni operates primarily outside city centres.

Food is positioned as part of a wider value-led shopping trip.

Market position

Tokmanni is not a full-service supermarket competitor.

However, its grocery volumes are meaningful in dry food, beverages, and household staples.

Operational relevance

- High demand for cost-efficient packaging

- Focus on private label and import sourcing

- Growing relevance for value-oriented suppliers

Tokmanni is increasingly visible in supplier tenders for commodity categories.

5. Minimani

Minimani is a Finnish-owned hypermarket operator founded in 2005.

It operates a very small but distinctive network.

Despite only 0.5% market share, Minimani has strong regional importance.

Core format

- Large hypermarkets with extended non-food ranges

Scale and operations

- 7 stores

- €123m in grocery sales

- ~350 employees

Each store generates high sales per unit compared with national averages.

Market position

Minimani focuses on destination shopping.

Its scale limits national influence, but local supplier relationships can be significant.

Operational relevance

- Large single-site volumes

- Flexible sourcing

- Opportunity-driven assortment planning

Minimani is often relevant for regional or niche suppliers rather than multinational brands.

Market structure impact

Finland’s grocery market structure creates a clear power imbalance.

Two groups control more than 80% of sales.

This concentration affects every layer of the supply chain.

Impacts include:

- Strong buyer leverage on pricing

- Standardised logistics requirements

- High compliance expectations

- Limited alternative routes to market

For suppliers, losing access to one of the top two groups can be commercially critical.

Category dominance trends

Certain categories are particularly influenced by concentration.

Private label

Private label penetration is high and rising.

S Group and K Group both operate multi-tiered private label portfolios.

Fresh food

Domestic sourcing remains strong.

However, centralised buying has reduced the number of approved suppliers.

Packaged grocery

Scale favours large manufacturers.

Smaller brands face higher listing thresholds and limited shelf space.

Industry direction

Several trends are shaping the next phase of Finnish grocery retail.

- Continued private label expansion

- Increased automation in distribution centres

- Tighter sustainability and packaging requirements

- Slower store network growth, more optimisation

Market share shifts are expected to be incremental rather than disruptive.

The top five structure is unlikely to change in the medium term.

Structural outlook

Finland’s grocery retail market will remain concentrated.

Barriers to entry are high.

Logistics costs, compliance demands, and scale requirements limit new challengers.

For suppliers and service providers, understanding the priorities of these five groups is essential.

Most commercial outcomes in Finland are decided within this narrow group of operators.

Conclusion

Finnish grocery retail is dominated by a small number of powerful supermarket groups.

S Group and K Group define the market.

Lidl provides sustained price pressure.

Tokmanni and Minimani occupy specific value-driven and regional roles.

This structure shapes the wider Finland FMCG environment, influencing buying power, category access and supply chain design across the country. It also reinforces the strength of Finland private label programmes, which continue to expand across core food and everyday categories.

Future change is expected to be gradual, not structural.

Editor’s Note: This article is based on publicly available company disclosures, industry statistics, and financial reports from FY2024–FY2025.