Poland is famous for apples, blueberries, raspberries and mushrooms. It is the largest apple producer in the European Union and one of Europe’s leading exporters of cultivated mushrooms and soft berries. Carrots, onions, cabbage and greenhouse tomatoes are also produced at large commercial scale, supplying both domestic supermarkets and cross-border EU retail chains.

Fresh fruit and vegetables are among the most in-demand grocery categories in Poland. Internationally, Polish apples and mushrooms define the country’s agricultural export profile. Blueberries have become a fast-growing high-value segment over the past decade.

The fresh produce companies in Poland that lead this sector are not defined only by revenue. Market influence is shaped by orchard acreage, greenhouse capacity, storage infrastructure, export reach and integration with supermarket logistics systems.

This ranking applies a hybrid structural model, assessing Polish-owned fresh produce companies based on production depth, export scale and operational relevance within European grocery supply chains.

10 Polish-Owned Fresh Produce Companies

| Rank | Company | Founded | Core Strength | Employees* | Structural Position |

|---|---|---|---|---|---|

| 1 | Appolonia Group | 2001 | Apples & exports | 600+ (seasonal incl.) | Major apple exporter |

| 2 | Rajpol Group | 1996 | Apple production | 500+ | EU retail supply |

| 3 | La-Sad | 2002 | Apple grower cooperative | 400+ | Large orchard base |

| 4 | Polskie Jagody | 2007 | Blueberries | 300+ | Leading berry exporter |

| 5 | Grupaproducentów Owoców Galster | 2003 | Apples | 250+ | Integrated packing |

| 6 | Green Factory | 2010 | Ready-to-eat salads | 700+ | Retail processing integration |

| 7 | Grupa Mularski | 1994 | Mushrooms | 600+ | EU mushroom exporter |

| 8 | Amplus Sp. z o.o. | 1992 | Fruits & vegetables distribution | 800+ | Retail logistics integration |

| 9 | Citronex Fresh | 1998 | Greenhouse tomatoes & bananas | 1,000+ | Controlled greenhouse scale |

| 10 | Grupaproducentów Owoców King Fruit | 2004 | Apples | 200+ | Export-aligned orchard base |

*Employee figures include seasonal labour where applicable. Data based on publicly available disclosures and company materials (FY2024–FY2025 where available).

1. Appolonia Group

Founded in 2001, Appolonia Group is one of Poland’s largest apple producer organisations.

Core categories:

Fresh apples

Export-grade varieties

Storage & controlled atmosphere facilities

Poland remains Europe’s largest apple producer, and Appolonia plays a central role in export logistics to Germany, Scandinavia, the Middle East and Asia.

Operationally, the company integrates orchard production with advanced storage, grading and packaging systems, ensuring year-round supply to supermarket chains. Structural power comes from acreage scale and export consistency.

2. Rajpol Group

Established in 1996, Rajpol is a major apple producer and exporter with extensive orchard control.

Core categories:

Dessert apples

Retail-packed fruit

Export bulk shipments

Rajpol supplies EU retailers and operates modern sorting and packing facilities. Structural relevance comes from consistent volume and quality standardisation aligned with supermarket sourcing frameworks.

3. La-Sad

La-Sad is a producer group founded in 2002, focused on apple cultivation and export alignment.

Core categories:

Fresh apples

Storage & grading

Retail carton formats

The group manages large orchard acreage and advanced cold storage systems. Its structural importance lies in cooperative governance, ensuring stable supply contracts into EU retail networks.

4. Polskie Jagody

Founded in 2007, Polskie Jagody specialises in blueberries and berry exports.

Core categories:

Blueberries

Seasonal berries

Export packaging

Poland has emerged as one of Europe’s leading blueberry producers. Polskie Jagody supports cross-border supermarket supply during peak European berry season, reinforcing Poland’s expanding high-value fruit segment.

5. Galster Producer Group

Founded in 2003, Galster operates integrated apple production and packing facilities.

Core categories:

Apples

Storage services

Export alignment

Galster’s infrastructure includes controlled-atmosphere warehouses, ensuring extended shelf life for retail distribution. Structural relevance comes from supply reliability across fluctuating harvest conditions.

6. Green Factory

Established in 2010, Green Factory operates at the intersection of fresh produce and processing.

Core categories:

Ready-to-eat salads

Fresh-cut vegetables

Retail packaged greens

Unlike orchard-based exporters, Green Factory integrates washing, cutting and packaging facilities. This positions it structurally within supermarket chilled supply chains, linking agricultural production with FMCG-ready formats.

7. Grupa Mularski

Founded in 1994, Grupa Mularski is a major Polish mushroom producer.

Core categories:

Fresh mushrooms

Export shipments

Retail packaging

Poland is Europe’s leading mushroom exporter. Mularski’s production facilities support steady supply into Western European retailers, reinforcing Poland’s dominance in this niche fresh category.

8. Amplus

Founded in 1992, Amplus operates across fresh fruit and vegetable sourcing and distribution.

Core categories:

Apples

Carrots

Onions

Export vegetables

Amplus plays a logistical role linking growers to retail chains. Its scale and sorting infrastructure place it structurally within Poland’s supermarket supply ecosystem.

9. Citronex Fresh

Founded in 1998, Citronex is a diversified agricultural group.

Core categories:

Greenhouse tomatoes

Bananas (distribution)

Fresh vegetables

Citronex controls one of Poland’s largest greenhouse tomato operations. While also active in import distribution, its domestic production footprint reinforces Poland’s greenhouse expansion trend.

10. King Fruit Producer Group

Established in 2004, King Fruit is another structurally significant apple producer group.

Core categories:

Apples

Storage & export packaging

Its relevance lies in export orientation and orchard integration rather than brand recognition, reflecting the cooperative structure common in Polish fresh fruit production.

Structural Analysis: Market Impact

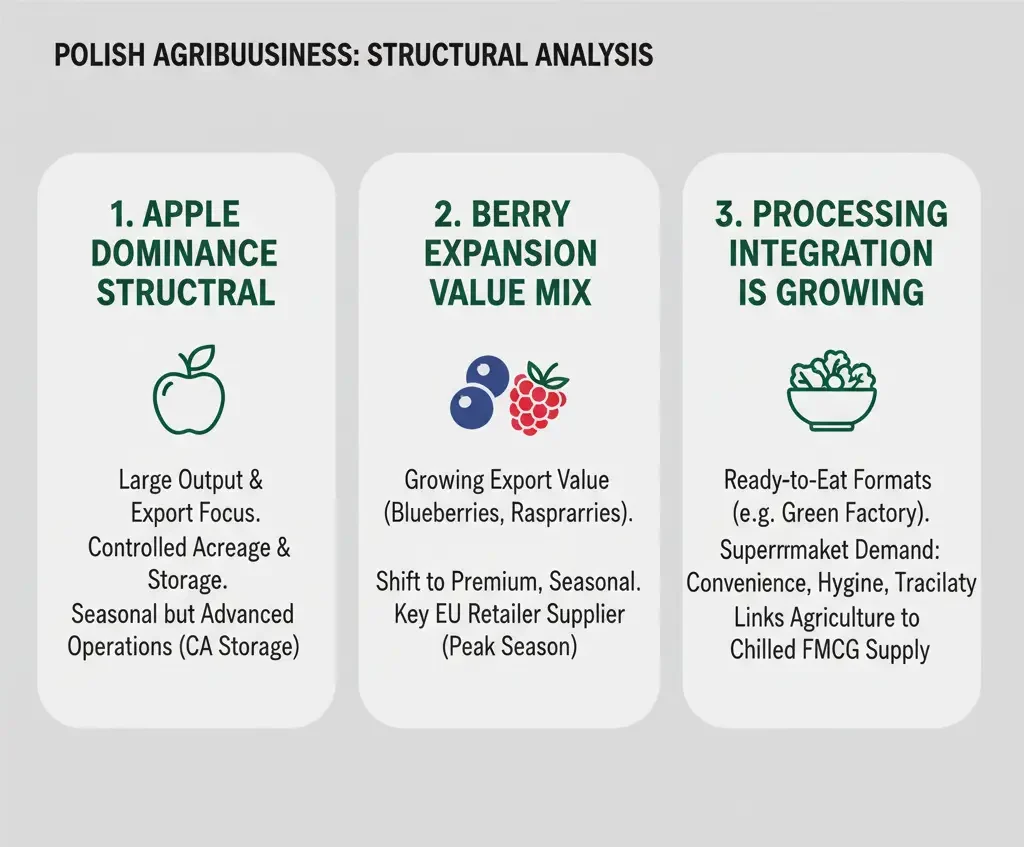

1. Apple Dominance Remains Structural

Apples account for a significant portion of Poland’s fresh fruit output. Producer groups control orchard acreage and storage infrastructure rather than operating as FMCG-style brands.

This concentration means export flows are highly seasonal but operationally advanced, supported by controlled atmosphere storage systems.

2. Berry Expansion Changes Value Mix

Blueberries and raspberries are gaining export value relative to apples.

Higher margin crops shift Poland’s fresh produce profile from volume-driven toward premium seasonal categories. Retailers increasingly rely on Poland during European berry season peaks.

3. Processing Integration Is Growing

Companies such as Green Factory demonstrate structural evolution toward ready-to-eat formats.

This integration reflects supermarket demand for convenience, hygiene certification and traceability, linking agriculture more closely to chilled FMCG supply chains.

Industry Direction (2026 Outlook)

Poland’s fresh produce structure is evolving in three key ways:

Increased greenhouse expansion to stabilise climate volatility

Higher certification requirements aligned with EU retail standards

Greater automation in sorting, grading and packaging

Labour availability and energy costs remain structural pressure points. However, export diversification beyond the EU is gradually expanding.

Market Structure Impact on Supermarkets

Polish fresh produce companies influence supermarket sourcing in Central and Western Europe through:

Volume reliability

Competitive pricing

Flexible packaging formats

EU-compliant certification systems

Supply chain efficiency, rather than brand recognition, defines competitive advantage.

Conclusion

Poland’s leading fresh produce companies in 2026 are defined by structural production scale, cooperative integration and export alignment rather than brand-driven revenue visibility. Apples remain dominant, but berries, mushrooms and greenhouse crops are reshaping value distribution across the national supply base.

For Poland supermarket networks, stability of volume and year-round storage capacity remain critical sourcing factors. Producer groups that control orchard acreage and cold-chain infrastructure are increasingly central to retail procurement strategies.

Across the wider Poland FMCG ecosystem, fresh categories are becoming more closely integrated with packaging standards, traceability systems and logistics automation. As compliance expectations rise across the EU, operational depth and export diversification will determine which producers retain structural influence within Poland’s fresh produce system.

Editor’s Note: This ranking is based on publicly available company disclosures, producer group information and sector data for FY2024–FY2025 where available. Employment figures may include seasonal workers. No currency conversion was required as revenue data was not uniformly disclosed.